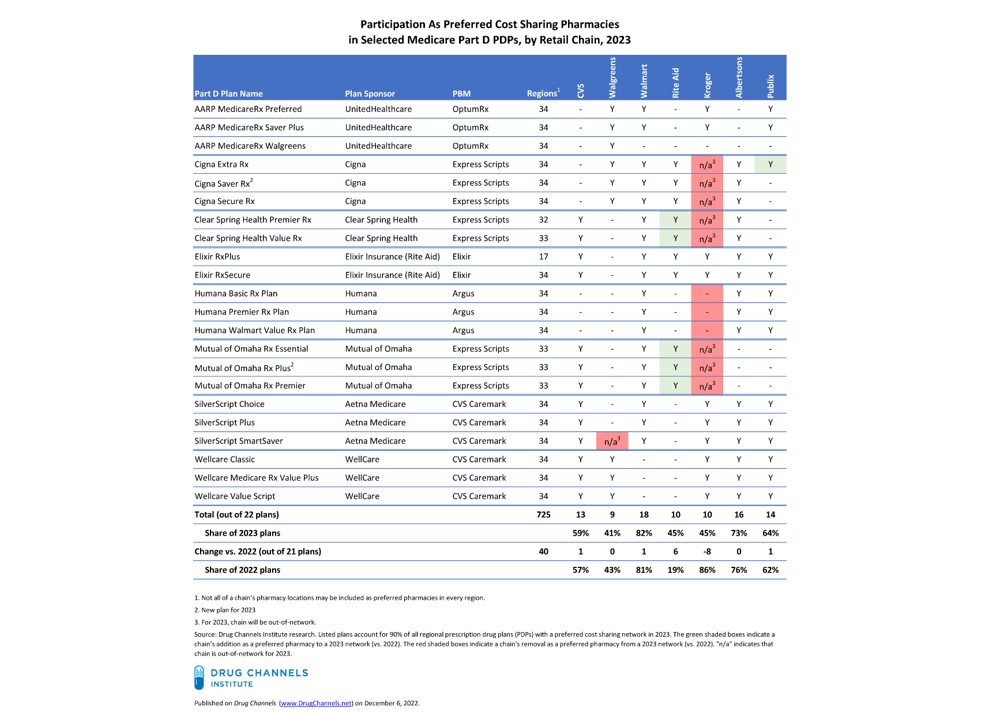

DCI’s exclusive analysis shows that 83% of seniors remain enrolled in PDPs with preferred pharmacy networks—essentially unchanged from 82% in 2025, but sharply lower than the 99% peak in 2023. Meanwhile, the number of major Part D plans offering preferred networks has fallen to a record-low eight.

The new enrollment data reveal a clear shift in competitive positioning: Albertsons and Publix are now preferred in every major plan. Walgreens is holding strong. Walmart—the company that invented the Part D preferred network model—has slipped to the middle of the preferred pack.

Meanwhile, smaller pharmacies have fully abandoned PDPs’ preferred networks in 2026.

At the same time, the IRA’s expansion of the Low-Income Subsidy (LIS) means a growing share of beneficiaries have little financial incentive to use a preferred pharmacy at all. Add in the PBM reforms in the Consolidated Appropriations Act of 2026, and the preferred network model will gradually lose relevance.

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: