This is my final post of 2006. I'm grateful for the positive response to my blog and very much appreciate the many positive emails and comments that I have received since launching 6 months ago.

Let's wrap-up the year with some homegrown Drug Channels supply chain humor, straight from the pages of The Wall Street Jovial:

I will be back with my outlook for 2007 on January 2. Until then, have a great holiday!

Adam

Drug Channels delivers timely analysis and provocative opinions from Adam J. Fein, Ph.D., the country's foremost expert on pharmaceutical economics and the drug distribution system. Drug Channels reaches an engaged, loyal and growing audience of more than 100,000 subscribers and followers. Learn more...

Friday, December 15, 2006

Wednesday, December 13, 2006

Catching up on AMP and PDMA

Here are a few noteworthy news items on AMP and PDMA that I want to recommend:

1. Roundtable: Deficit Reduction Act (Pharmaceutical Executive, Nov. 2006)

I believe that 2007 could go down as the year of Average Manufacturer Price (AMP). I still believe that AMP will ultimately have a much bigger impact than many people expect. (See my June post McClellan and the magic AMP for background.) This roundtable article has some good insights about:

2. Injunction May Slow Momentum for RFID E-Pedigrees (RFID Update, Dec. 12 2006)

Check out this interesting article on PDMA that quotes Jayne Juvan, my favorite (and the only?) healthcare law blogger, as saying: "Ultimately, the courts tend to favor the government in cases such as this that allege Equal Protection Clause and Due Process Clause violations when the rational basis test applies." She's referring to the RxUSA et al case against the FDA.

The article also calls Drug Channels a "pharmaceutical law blog," which almost offends me. Maybe I should sue?

1. Roundtable: Deficit Reduction Act (Pharmaceutical Executive, Nov. 2006)

I believe that 2007 could go down as the year of Average Manufacturer Price (AMP). I still believe that AMP will ultimately have a much bigger impact than many people expect. (See my June post McClellan and the magic AMP for background.) This roundtable article has some good insights about:

- The class of trade issue

- The use of AMP for rebates vs. reimbursement

- Implications of a public release

2. Injunction May Slow Momentum for RFID E-Pedigrees (RFID Update, Dec. 12 2006)

Check out this interesting article on PDMA that quotes Jayne Juvan, my favorite (and the only?) healthcare law blogger, as saying: "Ultimately, the courts tend to favor the government in cases such as this that allege Equal Protection Clause and Due Process Clause violations when the rational basis test applies." She's referring to the RxUSA et al case against the FDA.

The article also calls Drug Channels a "pharmaceutical law blog," which almost offends me. Maybe I should sue?

Sunday, December 10, 2006

Thank You for Buying Counterfeits

Can’t get enough PDMA news?

Well, head over to Jayne Juvan’s surprisingly readable legal analysis of the recent injunction entitled RX USA Wholesale v. Department of Health & Human Services: A Legal Perspective. Jayne is a fan of yours truly, so allow me to return the compliment and suggest you read her thought-provoking perspective. She concludes: "Despite this victory, the Plaintiffs in this case have a long way to go, as the litigation only began a few months ago and this is only one hurdle among many that the Plaintiffs must overcome."

I was immediately reminded of a scene from the very funny movie Thank You for Smoking in which the main character (a Washington lobbyist) is asked by his son: "Dad, why is American government the best government?" Without looking up, Dad the lobbyist quickly replies:"Because of our endless appeals system." (This is a great DVD and an even funnier book, so make haste and pick it up today.)

More prosaically, I believe that the very concept of “pedigree” may need to be reconsidered. Counterfeits enter via diversion in the secondary market. But counterfeit sellers require counterfeit buyers, a problem that is not directly solved by pedigree requirements of the PDMA.

In Our Demand Side Counterfeit Drug Problem, I describe three rules that must be followed for pedigree to make the supply chain safer:

In response, the National Association of Boards of Pharmacy launched a new website in November called http://www.dangerouspill.com/, complete with self-congratulatory press release. Like its PhRMA-sponsored counterpart http://www.buysafedrugs.info/, the NABP site aims to educate consumers about the dangers of buying counterfeits.

Business Week also jumped on the bandwagon this week with Bitter Pills, an article outlining the dangers of ordering drugs from “shady online marketers.” (Good tip!) Business Week helpfully portrays the sordid world of online pill sales as a cartoon, although I don't think my kids will be seeing that cartoon on Nickelodean following The Fairly Oddparents!

These worthy efforts aim at consumers. But I must note that the NABP and PhRMA sites sidestep the culpability or responsibility for pharmacy buyers to follow safe sourcing practices. Yes, I know that the NABP Model Rules outline various “Criminal Acts” associated with knowingly handling counterfeit drugs. Even legitimate pharmacists sometimes purchase in the secondary market. For example, a 2004 study found that two-thirds of hospital pharmacy directors use secondary wholesalers as a resource to obtain needed supplies during a product shortage. (Source: A research article published in the American Journal of Health-System Pharmacists.)

The industry sites do not help consumers identify legitimate pharmacies nor do they provide a way to validate that a pharmacy is behaving ethically in its sourcing practices. “End-to-end” visibility is a long way off, so we in the industry must confront the pharmacy buyer problem sooner or later, regardless of the endless appeals that are likely to dog the FDA's attempts to implement the PDMA.

Well, head over to Jayne Juvan’s surprisingly readable legal analysis of the recent injunction entitled RX USA Wholesale v. Department of Health & Human Services: A Legal Perspective. Jayne is a fan of yours truly, so allow me to return the compliment and suggest you read her thought-provoking perspective. She concludes: "Despite this victory, the Plaintiffs in this case have a long way to go, as the litigation only began a few months ago and this is only one hurdle among many that the Plaintiffs must overcome."

I was immediately reminded of a scene from the very funny movie Thank You for Smoking in which the main character (a Washington lobbyist) is asked by his son: "Dad, why is American government the best government?" Without looking up, Dad the lobbyist quickly replies:"Because of our endless appeals system." (This is a great DVD and an even funnier book, so make haste and pick it up today.)

More prosaically, I believe that the very concept of “pedigree” may need to be reconsidered. Counterfeits enter via diversion in the secondary market. But counterfeit sellers require counterfeit buyers, a problem that is not directly solved by pedigree requirements of the PDMA.

In Our Demand Side Counterfeit Drug Problem, I describe three rules that must be followed for pedigree to make the supply chain safer:

- Pharmacy buyers must demand pedigree documents (electronic or paper) from wholesalers and be able to validate the authenticity of these documents.

- Pharmacy buyers must only purchase from wholesale distributors in the “Normal Distribution Channel” or wholesale distributors that are willing and able to supply pedigree.

- Consumers must (a) refuse to do business with any pharmacy that does not adhere to the preceding two rules, and (b) be able to validate a pharmacy’s compliance with these rules.

In response, the National Association of Boards of Pharmacy launched a new website in November called http://www.dangerouspill.com/, complete with self-congratulatory press release. Like its PhRMA-sponsored counterpart http://www.buysafedrugs.info/, the NABP site aims to educate consumers about the dangers of buying counterfeits.

Business Week also jumped on the bandwagon this week with Bitter Pills, an article outlining the dangers of ordering drugs from “shady online marketers.” (Good tip!) Business Week helpfully portrays the sordid world of online pill sales as a cartoon, although I don't think my kids will be seeing that cartoon on Nickelodean following The Fairly Oddparents!

These worthy efforts aim at consumers. But I must note that the NABP and PhRMA sites sidestep the culpability or responsibility for pharmacy buyers to follow safe sourcing practices. Yes, I know that the NABP Model Rules outline various “Criminal Acts” associated with knowingly handling counterfeit drugs. Even legitimate pharmacists sometimes purchase in the secondary market. For example, a 2004 study found that two-thirds of hospital pharmacy directors use secondary wholesalers as a resource to obtain needed supplies during a product shortage. (Source: A research article published in the American Journal of Health-System Pharmacists.)

The industry sites do not help consumers identify legitimate pharmacies nor do they provide a way to validate that a pharmacy is behaving ethically in its sourcing practices. “End-to-end” visibility is a long way off, so we in the industry must confront the pharmacy buyer problem sooner or later, regardless of the endless appeals that are likely to dog the FDA's attempts to implement the PDMA.

Wednesday, December 06, 2006

The Impact of the PDMA Injunction

What will the injunction against the Prescription Drug Marketing Act (PDMA) mean in the pharmaceutical industry? (For background, see No PDMA for you! and It's Official: PDMA is Back On Hold.)

The FDA has not updated their PDMA resources page as of this morning, so it’s unclear what their formal strategy will be. Since I’m not qualified to opine on the FDA’s legal options, I’ll focus on a few business implications for manufacturers and wholesalers.

Manufacturers

This injunction should serve as a channel strategy wake-up call to manufacturers. In my opinion, senior executives in commercial operations at pharmaceutical companies should push their trade relations teams to develop formal channel management strategies. Frankly, the PDMA’s conception of “authorized distributor of record” is somewhat simplistic relative to channel management practices in other industries. (More on this topic below.)

I also want to reinforce my belief that manufacturers should invest more resources into gaining visibility into the movement of their product from factory to patient. Despite the RFID hype, the U.S. is still many years from a functional track-and-trace infrastructure, which was defined by Dr. von Eschenbach as “from the assembly line to the dispenser” at the NACDS/HDMA RFID conference. (See The FDA on PDMA.)

The Secondary Market

Let’s not delude ourselves –secondary markets will always exist when there are opportunities to arbitrage price differences between identical products being sold at different prices in different markets. In Europe, this arbitrage occurs as products are diverted across national borders and is called parallel trade. (See London Calling: Fake Drugs Get Real.) In the U.S., arbitrage also occurs as products are diverted between different classes of trade. Check out this graphical depiction of gateways into the U.S. supply chain.

While diverted or resold products are not necessarily counterfeits, all counterfeits enter via diversion in the secondary market. As the Chairman of the Subcommittee on Criminal Justice, Drug Policy and Human Resources noted in November 2005: “The FDA confirmed with Subcommittee staff that drug diversion was the entry point for every case investigated by that agency involving counterfeit drugs going into legitimate pharmacies.” Thus, any wholesaler operating in the secondary market should reasonably expect a higher level of scrutiny over their activities.

Secondary wholesalers

I am impressed by this legal victory, especially given my earlier skepticism. However, secondary wholesalers should recognize that manufacturers in many industries can and do legitimately limit the number of intermediaries that are authorized to sell its products. For example, Apple only allows iPods to be sold through authorized resellers.

The degree of distribution selectivity is a strategic channel design issue for a manufacturer, ranging from a single distributor (exclusivity) to an unrestricted number of distributors within a given market (intensive distribution). There is a large body of academic research on distribution channel selectivity in economics, law, and marketing supporting these channel strategies. Fans of academic jargon may enjoy reading an academic research paper on the topic that I published almost 10 years ago (available here), although the data did not include the pharmaceutical industry.

Given my comments about diversion above, secondary wholesalers must be willing to provide complete transparency to manufacturers about their business practices and product sources. Legitimate secondary wholesalers must be willing to clearly and unequivocally demonstrate how they differ from the unsavory wholesalers that traffic in potentially counterfeit product.

Big 3 Wholesalers

I believe that the introduction of Inventory Management Agreements (IMAs) and Fee-for-Service agreements now limit product leakage into the grey market, closing a significant entry point for counterfeiters. Drug makers literally pay for greater product security by purchasing data from wholesalers to monitor orders, inventories, and product movement in real-time.

In addition, wholesalers such as AmerisourceBergen Corp (ABC) and Cardinal Health Inc (CAH) publicly renounced secondary market sourcing, the HDMA tightened its membership requirements, and major pharmacy chains such as CVS committed to secure sourcing. My conversations with executives at the big 3 wholesalers – McKesson Corp (MCK), Cardinal Health, and AmerisourceBergen – have convinced me that these companies are genuinely committed to a secure supply chain.

Two more things

The FDA has not updated their PDMA resources page as of this morning, so it’s unclear what their formal strategy will be. Since I’m not qualified to opine on the FDA’s legal options, I’ll focus on a few business implications for manufacturers and wholesalers.

Manufacturers

This injunction should serve as a channel strategy wake-up call to manufacturers. In my opinion, senior executives in commercial operations at pharmaceutical companies should push their trade relations teams to develop formal channel management strategies. Frankly, the PDMA’s conception of “authorized distributor of record” is somewhat simplistic relative to channel management practices in other industries. (More on this topic below.)

I also want to reinforce my belief that manufacturers should invest more resources into gaining visibility into the movement of their product from factory to patient. Despite the RFID hype, the U.S. is still many years from a functional track-and-trace infrastructure, which was defined by Dr. von Eschenbach as “from the assembly line to the dispenser” at the NACDS/HDMA RFID conference. (See The FDA on PDMA.)

The Secondary Market

Let’s not delude ourselves –secondary markets will always exist when there are opportunities to arbitrage price differences between identical products being sold at different prices in different markets. In Europe, this arbitrage occurs as products are diverted across national borders and is called parallel trade. (See London Calling: Fake Drugs Get Real.) In the U.S., arbitrage also occurs as products are diverted between different classes of trade. Check out this graphical depiction of gateways into the U.S. supply chain.

While diverted or resold products are not necessarily counterfeits, all counterfeits enter via diversion in the secondary market. As the Chairman of the Subcommittee on Criminal Justice, Drug Policy and Human Resources noted in November 2005: “The FDA confirmed with Subcommittee staff that drug diversion was the entry point for every case investigated by that agency involving counterfeit drugs going into legitimate pharmacies.” Thus, any wholesaler operating in the secondary market should reasonably expect a higher level of scrutiny over their activities.

Secondary wholesalers

I am impressed by this legal victory, especially given my earlier skepticism. However, secondary wholesalers should recognize that manufacturers in many industries can and do legitimately limit the number of intermediaries that are authorized to sell its products. For example, Apple only allows iPods to be sold through authorized resellers.

The degree of distribution selectivity is a strategic channel design issue for a manufacturer, ranging from a single distributor (exclusivity) to an unrestricted number of distributors within a given market (intensive distribution). There is a large body of academic research on distribution channel selectivity in economics, law, and marketing supporting these channel strategies. Fans of academic jargon may enjoy reading an academic research paper on the topic that I published almost 10 years ago (available here), although the data did not include the pharmaceutical industry.

Given my comments about diversion above, secondary wholesalers must be willing to provide complete transparency to manufacturers about their business practices and product sources. Legitimate secondary wholesalers must be willing to clearly and unequivocally demonstrate how they differ from the unsavory wholesalers that traffic in potentially counterfeit product.

Big 3 Wholesalers

I believe that the introduction of Inventory Management Agreements (IMAs) and Fee-for-Service agreements now limit product leakage into the grey market, closing a significant entry point for counterfeiters. Drug makers literally pay for greater product security by purchasing data from wholesalers to monitor orders, inventories, and product movement in real-time.

In addition, wholesalers such as AmerisourceBergen Corp (ABC) and Cardinal Health Inc (CAH) publicly renounced secondary market sourcing, the HDMA tightened its membership requirements, and major pharmacy chains such as CVS committed to secure sourcing. My conversations with executives at the big 3 wholesalers – McKesson Corp (MCK), Cardinal Health, and AmerisourceBergen – have convinced me that these companies are genuinely committed to a secure supply chain.

Two more things

- Before we let the rhetoric about “extinction of small distributors” get out of hand, I must ask: How come we have not heard about secondary wholesalers going out of business in Florida after the July 1 implementation of state-level pedigree? Just wondering…

- I must be touching a nerve on this topic because a few individuals prefer to insult me via private emails. One of these fellows (“D.K.”) is too cowardly to disclose his affiliation in this matter. I have posted my opinions for all to see. Perhaps he will open himself up to the same scrutiny by posting a (non-anonymous) comment on this blog.

Tuesday, December 05, 2006

It's Official: PDMA is Back On Hold

The pedigree requirements of the Prescription Drug Marketing Act (PDMA) are back on hold. This is a big loss for the FDA and a big win for secondary wholesalers, especially RxUSA. I'll post tomorrow on possible implications for the pharmaceutical supply chain in 2007.

See my post from last Friday -- No PDMA for You! -- for background. Then read Federal Injunction Will Delay Part of Drug-Tracking Law in today's Wall Street Journal, which states:

"In a surprising decision that strikes a blow against Food and Drug Administration efforts to curb counterfeit drugs, a federal judge granted an injunction that delays part of a long-stalled drug law that was to have taken effect Friday of last week.

Yesterday, U.S. District Court Judge Joanna Seybert of the Eastern District of New York sided with a group of drug wholesalers who argued that the law is in breach of equal protection and due process because it requires certain recordkeeping of some wholesalers but not others, according to lawyers for both sides of the case."

BTW, Heather Won Tesoriero of the WSJ and I appear to be the only people writing about this topic. Although that's surprising given the hype leading up to Dec. 1, I think of it as just one more good reason to tell your friends in the industry to read this blog. 'nuff said.

See my post from last Friday -- No PDMA for You! -- for background. Then read Federal Injunction Will Delay Part of Drug-Tracking Law in today's Wall Street Journal, which states:

"In a surprising decision that strikes a blow against Food and Drug Administration efforts to curb counterfeit drugs, a federal judge granted an injunction that delays part of a long-stalled drug law that was to have taken effect Friday of last week.

Yesterday, U.S. District Court Judge Joanna Seybert of the Eastern District of New York sided with a group of drug wholesalers who argued that the law is in breach of equal protection and due process because it requires certain recordkeeping of some wholesalers but not others, according to lawyers for both sides of the case."

BTW, Heather Won Tesoriero of the WSJ and I appear to be the only people writing about this topic. Although that's surprising given the hype leading up to Dec. 1, I think of it as just one more good reason to tell your friends in the industry to read this blog. 'nuff said.

Monday, December 04, 2006

Sloppy reporting about Wal-Mart

Last Thursday's New York Times included some very sloppy reporting about Wal Mart Stores Inc (WMT). See Side Effects at the Pharmacy. (The story was widely syndicated, so here's an alternate link: Side Effects at the Pharmacy.)

The article questions the profitability of Wal-Mart’s program by incorrectly interpreting prescription data and then quoting a “consultant” with an undisclosed bias against Wal-Mart. This type of shoddy reporting only further confuses the debate about health care spending.

Since the New York Times’ editors read this blog, allow me to clear the air a bit by answering four questions:

- How busy is an average Wal-Mart pharmacy? (A: A lot less than an average Walgreens)

- How many more prescriptions did the $4 generic program generate? (A: About 16% more)

- Did Wal-Mart have $31.5 million in extra dispensing costs? (A: Nope.)

- Why was the Times so unbalanced? (A: Piling on?)

Q1: How busy is an average Wal-Mart pharmacy?

As a baseline, let’s estimate the typical volume at a Wal-Mart pharmacy in 2005.

- According to Drug Store News, Wal-Mart’s 2005 Rx sales were $11.036 billion.

- The average price per script in the mass merchant pharmacies was $62, implying that Wal-Mart dispensed 178 million prescriptions in 2005.

- Wal-Mart had 3,289 stores with pharmacies (per DSN).

After a little math, I estimate that the average Wal-Mart store dispensed 148 prescriptions per day in 2005 (assuming 365 selling days per year). For comparison, the same calculation for Walgreens yields an estimate of 270 prescriptions per pharmacy per day in 2005.

Q2: How many more prescriptions did the $4 generic program generate?

According to Wal-Mart’s Nov. 16 press release: “To date, as new states have been added to the program, 2.1 million more new prescriptions have been filled in those states as compared to the same time periods last year.”

- As of November 15, the generics program was available in 2,507 Wal-Mart stores.

- Stores were added on four different days (9/21; 10/6; 10/19; and 10/26). A calendar and some math shows that Wal-Mart had almost 65,000 total available selling days for the $4 generics program in these stores.

- Wal-Mart’s claim of “2.1 million more new prescriptions” translates into almost 15,000 new prescriptions per available selling day, or 32 new prescriptions per store per available selling day.

In other words, the average Wal-Mart pharmacy’s daily volume has increased by 22% (32/148) from September 21 to November 15.

However, IMS data indicates that total prescription growth was 6% from mid-September to mid-November 2006 versus the same period last year.

Therefore, it appears that Wal-Mart’s $4 generic program has added about 16% in real incremental prescription volume to the typical Wal-Mart pharmacy.

Q3: Did Did Wal-Mart have $31.5 million in extra dispensing costs?

The New York Times pooh-poohs the program, noting “…Wal-Mart might be able to declare the overall program profitable only by spreading the costs well beyond its pharmacy ledger.” The reporter then quotes “a pharmacy consultant in Stoughton, Wis.” named Ed Heckman: “But other costs, including store overhead and pharmacists’ paychecks, can add as much as $15 to the cost of dispensing a prescription, Mr. Heckman said. ”

Let’s see…2.1 million prescriptions @ $15 equals …$31.5 million!! So the program must be a boon for all of those pharmacists who are working extra hours, right?

Wrong. Total volume at a Wal-Mart pharmacy has gone up by about 32 new prescriptions per day – about 2 per hour given typical store hours. Marginal (incremental) overhead costs are probably $0.00 for an average Wal-Mart pharmacy. Following Mr. Heckman’s quote, the reporter notes that “selling drugs at $4 might be well below cost for many pharmacies.” Perhaps, but probably not for Wal-Mart.

Q4: Why was the Times so unbalanced?

I’m afraid I can’t really answer this question. Perhaps they are piling on after the post-election bashing given by Senator Barack Obama and former Senator John Edwards?

Nevertheless, I feel compelled to note that the New York Times failed to disclose a major conflict behind the quote above about costs. Mr. Heckman is not just a “pharmacy consultant,” but also President of PAAS National, a company that is "supported and endorsed by the NCPA” (the National Community Pharmacists Association). According to its website, PAAS also operates the Community Pharmacy Contract Clearinghouse for NCPA.

I note this lack of disclosure because NCPA has been a very outspoken critic of Wal-Mart. Check out the rather unambiguous titles of NCPA’s press releases "analyzing" Wal-Mart's $4 program:

- Wal-Mart Generics Program: Less Than Meets The Eye (11/21/06)

- Wal-Mart PR Stunt Goes Nationwide (10/19/06)

- Wal-Mart Pulls Another Fast One (10/5/06)

- Wal-Mart Offers Up Classic Bait-and-Switch (9/28/06)

Hmmm, wonder what NCPA really thinks?

---

Anyway, this point of this post is simply to highlight that sometimes what passes for analysis in the mainstream media is really just opinion. Or as U.S. Senator Daniel Patrick Moynihan famously quipped: "Everyone is entitled to his own opinion, but not his own facts."

Friday, December 01, 2006

No PDMA for you!

Looks like the PDMA will not be going into effect after all.

Looks like the PDMA will not be going into effect after all.I've been skeptical about the injunction filed by a group of secondary wholesalers to stop implementation of the pedigree requirements of the PDMA on Dec. 1. (See The FDA on PDMA and Channel Conflict as Pedigree Looms.)

But on Thursday, Magistrate Judge Kathleen Tomlinson recommended that a preliminary injunction against the Department of Health and Human Services and the FDA be granted. See the Wall Street Journal story Judge Rules on Long-Delayed Drug Law. (Fans of legal reasoning will surely enjoy the full injunction report and recommendation.)

Sunday, November 26, 2006

Of Spammers and Senators

Have you ever wondered where spammers get their counterfeit Viagra? Or why U.S. Senators don’t care?

If so, then you should check out The Philadelphia Inquirer’s fascinating 8-part series about a father-son duo that imported bulk drugs from India and then fulfilled orders for online pharmacies. Check it out here: http://go.philly.com/drugnet

Here’s how it worked:

Nevertheless, I’d be willing to wager that manufacturing conditions at Dr. Bansal’s Indian operation did not quite meet FDA GMP standards. No mention of distribution best practices in the Queens warehouse, either.

The Return of Cosmic Irony

And in a strange bit of cosmic irony, the Associated Press put a prescription drug reimportation story on the wires Thursday. See New push to allow imported drugs expected in Congress.

Unfortunately, Senators Vitter and Nelson remain blissfully ignorant about the dangers posed by allowing consumers to source products outside of legitimate domestic channels. Some questions for them:

--

On a happier note, Jayne Juvan, the legal brains behind Juvan's Health Law Update, just made my Monday morning by recommending this blog to her readers. Thanks, Jayne! I'll do the same and suggest that you all check out Jayne's weekly legal update.

If so, then you should check out The Philadelphia Inquirer’s fascinating 8-part series about a father-son duo that imported bulk drugs from India and then fulfilled orders for online pharmacies. Check it out here: http://go.philly.com/drugnet

Here’s how it worked:

- To avoid U.S. Customs, which targets small pill packages from overseas Web sites, Dr. Brij Bansal in India and his son, Akhil Bansal in Philadelphia, shipped millions of pills in bulk from Delhi to their Queens, N.Y., distribution center.

- American consumers, responding to spam or using Google to search for drugs, placed a credit-card order with a Web site. The Web site charged the consumer's credit card, then forwarded the order to the Bansals’ operations in Agra, India, and Queens.

- Immigrants at the Queens depot fulfilled the order, stuffing pills inside envelopes for UPS pickup. Within a day or two, UPS delivered the pills to the consumer's doorstep. Every few weeks, the Web-site operators wired payment to one of Akhil Bansal's bank accounts.

Nevertheless, I’d be willing to wager that manufacturing conditions at Dr. Bansal’s Indian operation did not quite meet FDA GMP standards. No mention of distribution best practices in the Queens warehouse, either.

The Return of Cosmic Irony

And in a strange bit of cosmic irony, the Associated Press put a prescription drug reimportation story on the wires Thursday. See New push to allow imported drugs expected in Congress.

Unfortunately, Senators Vitter and Nelson remain blissfully ignorant about the dangers posed by allowing consumers to source products outside of legitimate domestic channels. Some questions for them:

- Where will "Canadian" pharmacies source products from? Hopefully not people like the Bansals, but we’ll never really know.

- How will we stop consumers from buying from “bad” pharmacies? I bet the Bansal’s online pharmacy customers had Canadian flags on their websites.

- Who will regulate non-U.S. pharmacies? The FDA does not regulate or control the buying practices of domestic retail pharmacies. Fans of reimportation have yet to explain how a U.S. government agency will ensure the safety of foreign sources. And keep in mind that the DEA, not the FDA, went after the Bansals.

--

On a happier note, Jayne Juvan, the legal brains behind Juvan's Health Law Update, just made my Monday morning by recommending this blog to her readers. Thanks, Jayne! I'll do the same and suggest that you all check out Jayne's weekly legal update.

Tuesday, November 21, 2006

The Attack on Generic Profits in Drug Channels

Today’s Wall Street Journal has a very good overview of key issues for the generic industry, such as biogenerics and the FDA’s generic approval process. See Democrats’ RX? Generics.

However, I wonder if this renewed political focus on generics will ultimately reduce the profits of pharmacy chains and wholesalers. Companies that could be affected include CVS Corp (CVS), Walgreens (NYSE WAG), and McKesson Corp (MCK), to name just a few.

As faithful readers of this blog know, the supply chain – wholesalers, retail pharmacies, and mail order – get a larger share of total prescription drug revenue from generics. Profits on generic drugs now subsidize the retail and wholesale distribution of much more expensive branded products. (See my May post Will unbundling crush pharmacy profits?).

How profitable are generics? For fun (?), I went back to the 2004 CBO report Medicaid’s Reimbursements to Pharmacies for Prescription Drugs, which studied Gross Profits per Script (GPS) for pharmacies under the Medicaid system. Note that the study refers to GPS as “markups” and excludes any co-payments received from patients.

Gross Profit Per Script for Pharmacies in Medicaid (2002)

- Brand-name Drugs = $13.80 (14%)

- Older Generic Drugs (pre-1997 launch) = $9.90 (70%)

- Newer Generic Drugs (1997 to 2002) launch = $32.10 (70%)

In other words, filling a generic Medicaid prescription earned a pharmacy $18.30 more per script in 2002. These data come from 2002, so they go a long way to explaining why the new Federal Upper Limit for generic reimbursement under Medicaid will shift to Average Manufacturer Price (AMP) + 250% rather than an AWP-minus model. (See McClellan and the Magic AMP and AWP Ain’t What Matters for background.)

The channel's genertic profits are also under visible attack in the minds of consumers. As I pointed out yesterday, Wal Mart Stores Inc (WMT) is aiming at the pharmacy industry’s weak spot, encouraging pharmacies to argue that consumers should ignore price. (See Wal-Mart Raises the Stakes.)

But let's not forget that these profit margins provide powerful incentives for generic substitution by the channel, which has in turn lowered drug spending by employers and the government. Key scenario questions that I am now considering with my clients:

- How will manufacturers and payers manage the costs of getting products from the factory to the patient?

- What will happen to the retail and wholesale channel if generic margins come down?

- What parts of the supply chain will retain reasonable profit opportunities?

Hey, I’m just one voice out there, so please don’t forget Newton’s Second Law of Consulting: For every expert, there is an equal and opposite expert.

Have a Happy Thanksgiving!

Monday, November 20, 2006

Wal-Mart Raises the Stakes

Does anyone still believe that Wal-Mart will not shake up the pharmacy industry?

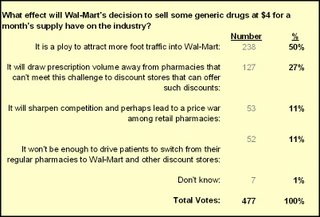

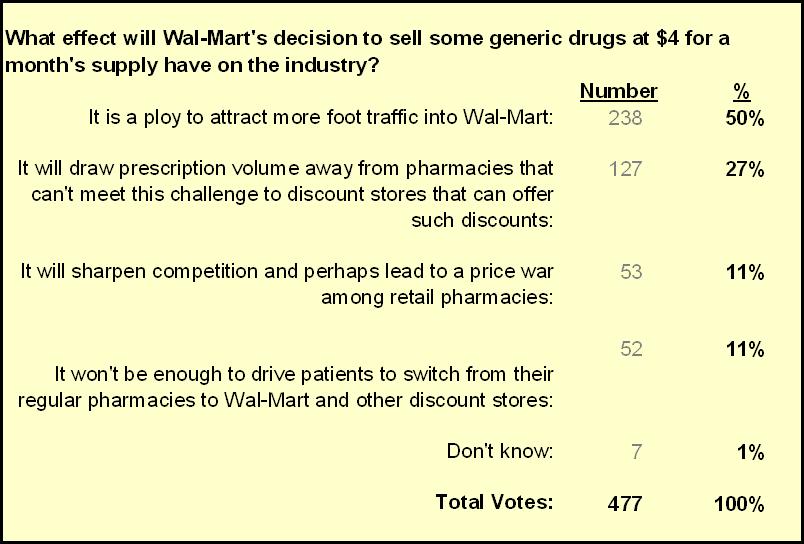

Wal Mart Stores Inc (WMT) just expanded its $4 generic program to 38 states and more than 3,000 pharmacies. See Wal-Mart Adds 11 More States To $4 Prescription-Drug Plan. Check out Bob Nease’s succinct overview of Wal-Mart’s updated list at Libratto.

Most interesting is the fact that Wal-Mart added pravastatin (generic Pravachol), a $2.3 billion blockbuster for Bristol-Myers Squibb Co (BMY) in 2005. Sounds like The Empire Strikes Back scenario in which I predicted that the list would be broadened to include blockbuster generics. In an online poll, that scenario got 56% of the votes vs. 44% for Much Ado About Nothing. (I stopped the voting after two weeks, so last week’s news did not affect the results.)

According to Wal-Mart’s press release: “To date, as new states have been added to the program, 2.1 million more new prescriptions have been filled in those states as compared to the same time periods last year.” If true, then Wal-Mart is increasing its average number of scripts per pharmacy by about 20% per store. I suspect that incremental costs for this additional volume are relatively low at Wal-Mart, making the program a financial win.

So far, no one has any real data on which chain or format is being affected by Wal-Mart. Most obviously, cash pay customers will switch first. Chains appear less vulnerable because customers with third-party insurance may not save very much versus standard co-pays.

However, chains are now in the awkward position of telling customer to ignore price, an argument that seems curiously at odds with the trend toward consumer-driven health care decision making. Walgreens (NYSE WAG) took the bait and issued a bizarre press release telling customers to focus on “convenient locations, close-in parking and unique pharmacy services.” Ouch. How long until CVS Corp (CVS) or Walgreens cave in and lower their generics margins? PBMs also risk a margin squeeze if payers question their generic dispensing profits versus Wal-Mart.

Bottom line: I stick by my prediction made when the plan was first announced in September: Wal-Mart's Generic Pricing Will Trigger Big Changes. My two criteria for the magnitude of the near-term impact were (a) how well Wal-Mart rolls out the program, and (b) how quickly (if ever) they include more mainstream generic products. (See Reconsidering Wal-Mart -- but just a little.) The national roll-out has been very fast. I predict generic Zoloft and Zocor are not far behind.

Wal Mart Stores Inc (WMT) just expanded its $4 generic program to 38 states and more than 3,000 pharmacies. See Wal-Mart Adds 11 More States To $4 Prescription-Drug Plan. Check out Bob Nease’s succinct overview of Wal-Mart’s updated list at Libratto.

Most interesting is the fact that Wal-Mart added pravastatin (generic Pravachol), a $2.3 billion blockbuster for Bristol-Myers Squibb Co (BMY) in 2005. Sounds like The Empire Strikes Back scenario in which I predicted that the list would be broadened to include blockbuster generics. In an online poll, that scenario got 56% of the votes vs. 44% for Much Ado About Nothing. (I stopped the voting after two weeks, so last week’s news did not affect the results.)

According to Wal-Mart’s press release: “To date, as new states have been added to the program, 2.1 million more new prescriptions have been filled in those states as compared to the same time periods last year.” If true, then Wal-Mart is increasing its average number of scripts per pharmacy by about 20% per store. I suspect that incremental costs for this additional volume are relatively low at Wal-Mart, making the program a financial win.

So far, no one has any real data on which chain or format is being affected by Wal-Mart. Most obviously, cash pay customers will switch first. Chains appear less vulnerable because customers with third-party insurance may not save very much versus standard co-pays.

However, chains are now in the awkward position of telling customer to ignore price, an argument that seems curiously at odds with the trend toward consumer-driven health care decision making. Walgreens (NYSE WAG) took the bait and issued a bizarre press release telling customers to focus on “convenient locations, close-in parking and unique pharmacy services.” Ouch. How long until CVS Corp (CVS) or Walgreens cave in and lower their generics margins? PBMs also risk a margin squeeze if payers question their generic dispensing profits versus Wal-Mart.

Bottom line: I stick by my prediction made when the plan was first announced in September: Wal-Mart's Generic Pricing Will Trigger Big Changes. My two criteria for the magnitude of the near-term impact were (a) how well Wal-Mart rolls out the program, and (b) how quickly (if ever) they include more mainstream generic products. (See Reconsidering Wal-Mart -- but just a little.) The national roll-out has been very fast. I predict generic Zoloft and Zocor are not far behind.

Tuesday, November 14, 2006

New York Times editors read this blog!

I don't normally agree with the New York Times editorial page, but it looks like they agree with me.

On Monday morning, I posted CMS as a PDP: A Part D compromise? suggesting a compromise on Part D that could avoid a Presidential veto:

"Medicare beneficiaries will have the option, but not the obligation, to enroll in a national plan based on directly negotiated prices. The current system of regional PDPs will remain, in effect putting the government into competition with private plans."

On Tuesday morning, The New York Times ran an editorial called Lowering Medicare Drug Prices, which states:

"The approach that most appeals to us would direct the secretary of health and human services to set up one or more government-operated drug plans to compete with the private plans. "

Interesting coincidence, don't you think?

On Monday morning, I posted CMS as a PDP: A Part D compromise? suggesting a compromise on Part D that could avoid a Presidential veto:

"Medicare beneficiaries will have the option, but not the obligation, to enroll in a national plan based on directly negotiated prices. The current system of regional PDPs will remain, in effect putting the government into competition with private plans."

On Tuesday morning, The New York Times ran an editorial called Lowering Medicare Drug Prices, which states:

"The approach that most appeals to us would direct the secretary of health and human services to set up one or more government-operated drug plans to compete with the private plans. "

Interesting coincidence, don't you think?

Monday, November 13, 2006

The FDA on PDMA

I’m blogging to you live from my hotel at the NACDS/HDMA RFID conference so I can opine real-time on the FDA’s hot-off-the-press pedigree documents.

The FDA released its final Compliance Policy Guide (CPG) and PDMA Q&A this morning shortly after Acting FDA Commissioner Andrew von Eschenbach addressed the conference. (All documents are available from the FDA’s new PDMA Resources page.) Ilisa Bernstein, Director of Pharmacy Affairs at FDA, also gave a presentation describing the Q&A.

Naturally, it’s a treat to hear directly from the FDA on the day new guidelines are released, even if the comments did not stray too far from the published documents. Here are three points that I took away from the presentations:

In my last PDMA post, I speculated on three possible outcomes from the PDMA:

Mark Parrish, newly appointed as CEO of Healthcare Supply Chain Services at Cardinal Health Inc (CAH), stated at the conference that Cardinal will continue to service some of its existing secondary wholesaler customers after December 1. AmerisourceBergen Corp. (ABC) highlighted its intention to provide pedigrees in a press release this afternoon. ABC noted that “…customers are charged fees that allow the Company to recover the cost of generating the pedigrees.” (I’ve heard that the monthly pedigree service fee is $5,000 for the first ship-to location, and $1,000 for each additional location.)

RFI-Do or RFI-Don’t?

Dr. von Eschenbach said that track-and-trace means "from the assembly line to the dispenser." Unfortunately, this year's RFID conference has once again provided little substance on the use of RFID by pharmacies to authenticate inbound product.

This is the major unspoken limitation in using RFID to make the supply chain more secure: How do we stop pharmacy buyers and consumers from purchasing outside of a theoretically secure supply chain? I refer to this challenge as Our Demand Side Counterfeit Drug Problem. It's the pachyderm in the parlor. And unless we start getting real about this problem, then we won't really be meeting the FDA's needs or securing the supply chain.

The FDA released its final Compliance Policy Guide (CPG) and PDMA Q&A this morning shortly after Acting FDA Commissioner Andrew von Eschenbach addressed the conference. (All documents are available from the FDA’s new PDMA Resources page.) Ilisa Bernstein, Director of Pharmacy Affairs at FDA, also gave a presentation describing the Q&A.

Naturally, it’s a treat to hear directly from the FDA on the day new guidelines are released, even if the comments did not stray too far from the published documents. Here are three points that I took away from the presentations:

- No more stays – The PDMA will be implemented on December 1, 2006. Dr. von Eschenbach indicated that the agency is considering no further stays, casting serious doubt on the legal actions being pursued by some secondary drug wholesalers. (See my earlier post Channel Conflict as Pedigree Looms.)

- “Some must…all should” – Both FDA officials used the phrase “some must … all should” in their respective presentations. The PDMA excludes manufacturers and Authorized Distributors of Record (ADR) from the requirement to provide pedigree. To my ears, the phrase “… all should” indicates that the FDA does not want to see the ADR exclusion become a loophole to avoid pedigree.

- Manufacturers gain leverage – The PDMA makes ADR designation more important. Manufacturers could use the concept of a “written agreement” associated with an ADR to enshrine supply chain business requirements that might otherwise be covered in fee-for-service or distribution service agreements. I predict that ADR agreements will play a role in the next round of fee-for-service negotiations.

In my last PDMA post, I speculated on three possible outcomes from the PDMA:

- Wholesalers with an ADR relationship will pick up volume.

- Manufacturers will broaden their ADR networks.

- The marketplace will create a solution for pedigree.

Mark Parrish, newly appointed as CEO of Healthcare Supply Chain Services at Cardinal Health Inc (CAH), stated at the conference that Cardinal will continue to service some of its existing secondary wholesaler customers after December 1. AmerisourceBergen Corp. (ABC) highlighted its intention to provide pedigrees in a press release this afternoon. ABC noted that “…customers are charged fees that allow the Company to recover the cost of generating the pedigrees.” (I’ve heard that the monthly pedigree service fee is $5,000 for the first ship-to location, and $1,000 for each additional location.)

RFI-Do or RFI-Don’t?

Dr. von Eschenbach said that track-and-trace means "from the assembly line to the dispenser." Unfortunately, this year's RFID conference has once again provided little substance on the use of RFID by pharmacies to authenticate inbound product.

This is the major unspoken limitation in using RFID to make the supply chain more secure: How do we stop pharmacy buyers and consumers from purchasing outside of a theoretically secure supply chain? I refer to this challenge as Our Demand Side Counterfeit Drug Problem. It's the pachyderm in the parlor. And unless we start getting real about this problem, then we won't really be meeting the FDA's needs or securing the supply chain.

CMS as a PDP: A Part D compromise?

Today's Wall Street Journal has a great editorial by Alain Enthoven and Kyna Fong on the Democrats' plan to push for direct negotiations between Medicare and the drug companies. See Pelosi on Drugs.

Despite these logical arguments, “Direct negotiations” has a simple, populist appeal that is hard to ignore. Just consider the fact that the issue was only narrowly defeated in a Republican-controlled House and Senate. (See my July post The Part D direct negotiations movement for background.)

I predict that a new compromise will emerge to avoid the prospect of a Presidential veto. Here's a brief sketch of how it might work:

Happy Jack

Part D has proven to be a very popular program, judging by the many polls on the topic. According to the latest poll from the Wall Street Journal and Harris Interactive:

The Seeker

Yet the direct negotiations crowd ignores the risk that changing the structure will lower satisfaction by reducing choices. I worry that the Democrat’s emotional focus on squeezing a few theoretical pennies out of drug makers may blind them to this variety.

A big benefit of today’s structure is the choice created with the competitive system. I looked up the plans in my home zip code in Pennsylvania using CMS’ online Prescription Drug Plan Finder. I found 66 prescription plans for 2007 with monthly premiums ranging from $14.80 to $104.50 (average premium = $36). There is substantial variation in deductibles, cost sharing, and coverage in the gap. A national view is available in this handy summary from the Kaiser Foundation.

The range among my local 66 plans indicates that seniors have a lot of choices and can select a plan based on personal needs and individual situation. I suspect many seniors would not be happy in a one-size-fits-all plan. And as I pointed two weeks ago, direct negotiations may also throw the pharmacy industry into chaos and help Wal-Mart – true irony for Democrats! (See Are the Democrats helping Wal-Mart's Pharmacy?

If Medicare offered its own PDP, then the actual beneficiaries could decide whether the government's (presumably) lower prices are better than one of the other 66 options available. Seems fair to me.

It’s Not Enough

I also want to comment on the embedded assumption of direct negotiations -- lower pharma prices are automatically beneficial to society in the long run. This assumption is not as self-evident as it might appear.

To quote from the Amazon description of Richard Epstein's new book Overdose: “While critics of pharmaceutical companies call for ever more stringent controls on virtually every aspect of drug development and approval, Epstein cautions that the effect of such an approach will be to stifle pharmaceutical innovation and slow the delivery of beneficial treatments to the patients who need them.” (I am currently reading this dense, challenging book and will post a review sometime after my next long flight.)

Or as Peter Pitts as Drugwonks puts it: "to paraphrase Winston Churchill) our pharmaceutical patent system is the worst way to stimulate and support health care innovation – except for every other system." (See There’s a prize in every box!)

I recently attended a conference at which the keynote speaker made an off-hand remark that “drug prices are too expensive.” But as an economist, I must ask: “Too expensive compared to what?” Getting sick? Dying?

By all means, let's have a vigorous debate about how to make tough tradeoffs in health care. But is it naïve to think that mandating “lower” prices will not have unintended and potentially undesirable consequences.

Lunch is still not free.

---

P.S. Observant readers will recognize the subliminal plugs for my favorite new CD Endless Wire. Hope you buy before you get old!

Despite these logical arguments, “Direct negotiations” has a simple, populist appeal that is hard to ignore. Just consider the fact that the issue was only narrowly defeated in a Republican-controlled House and Senate. (See my July post The Part D direct negotiations movement for background.)

I predict that a new compromise will emerge to avoid the prospect of a Presidential veto. Here's a brief sketch of how it might work:

- Medicare beneficiaries will have the option, but not the obligation, to enroll in a national plan based on directly negotiated prices.

- The current system of regional PDPs will remain, in effect putting the government into competition with private plans.

- The government plan will receive an additional rebate analogous to the Medicaid rebate program, which seeks to ensure that Medicaid agencies pay the lowest (“best”) price available to any other customer.

Happy Jack

Part D has proven to be a very popular program, judging by the many polls on the topic. According to the latest poll from the Wall Street Journal and Harris Interactive:

- Three-quarters of enrollees say they are satisfied with the plan, compared with 24% who aren't satisfied.

- 70% say the plan has saved them money on prescription drugs, compared with 20% who say it hasn't.

- The plan has been easy to use, say 82% of respondents vs. 13% who disagree.

The Seeker

Yet the direct negotiations crowd ignores the risk that changing the structure will lower satisfaction by reducing choices. I worry that the Democrat’s emotional focus on squeezing a few theoretical pennies out of drug makers may blind them to this variety.

A big benefit of today’s structure is the choice created with the competitive system. I looked up the plans in my home zip code in Pennsylvania using CMS’ online Prescription Drug Plan Finder. I found 66 prescription plans for 2007 with monthly premiums ranging from $14.80 to $104.50 (average premium = $36). There is substantial variation in deductibles, cost sharing, and coverage in the gap. A national view is available in this handy summary from the Kaiser Foundation.

The range among my local 66 plans indicates that seniors have a lot of choices and can select a plan based on personal needs and individual situation. I suspect many seniors would not be happy in a one-size-fits-all plan. And as I pointed two weeks ago, direct negotiations may also throw the pharmacy industry into chaos and help Wal-Mart – true irony for Democrats! (See Are the Democrats helping Wal-Mart's Pharmacy?

If Medicare offered its own PDP, then the actual beneficiaries could decide whether the government's (presumably) lower prices are better than one of the other 66 options available. Seems fair to me.

It’s Not Enough

I also want to comment on the embedded assumption of direct negotiations -- lower pharma prices are automatically beneficial to society in the long run. This assumption is not as self-evident as it might appear.

To quote from the Amazon description of Richard Epstein's new book Overdose: “While critics of pharmaceutical companies call for ever more stringent controls on virtually every aspect of drug development and approval, Epstein cautions that the effect of such an approach will be to stifle pharmaceutical innovation and slow the delivery of beneficial treatments to the patients who need them.” (I am currently reading this dense, challenging book and will post a review sometime after my next long flight.)

Or as Peter Pitts as Drugwonks puts it: "to paraphrase Winston Churchill) our pharmaceutical patent system is the worst way to stimulate and support health care innovation – except for every other system." (See There’s a prize in every box!)

I recently attended a conference at which the keynote speaker made an off-hand remark that “drug prices are too expensive.” But as an economist, I must ask: “Too expensive compared to what?” Getting sick? Dying?

By all means, let's have a vigorous debate about how to make tough tradeoffs in health care. But is it naïve to think that mandating “lower” prices will not have unintended and potentially undesirable consequences.

Lunch is still not free.

---

P.S. Observant readers will recognize the subliminal plugs for my favorite new CD Endless Wire. Hope you buy before you get old!

Monday, November 06, 2006

CVS-Caremark: Why Now?

The CVS Corp (CVS) - Caremark Rx Inc (CMX) deal is raising many as-yet-unanswered questions about the timing of the deal.

Today’s Wall Street Journal article on Tom Ryan’s background (CVS's Deal Maker Faces Toughest Test Integrating Caremark) alludes to some of the investor discontent, noting: “Some Caremark shareholders are grumbling that the purchase price is too low; some wonder if the sale is driven by weakness in Caremark's business.” In contrast, the original article from last week (CVS, Caremark Unite to Create Drug-Sale Giant) focuses on the conflict-of-interest issues because it was co-written by Barbara Martinez.

Below are the four hypotheses that I am hearing in my conversations. Vote for your favorite (anonymously, of course). If you choose "None of the Above," please add comment to this post with your preferred explanation.

Hypothesis 1: Why not?

Given the strategic rationale for channel compression, a deal was inevitable at some point in the next few years. (My take was posted on Thursday as Consolidation of the US Pharmaceutical Infrastructure). In brief, CVS has been trying to get closer to employers and payers with Pharmacare. At the same time, Caremark has become a major dispensing pharmacy through its mail order and specialty pharmacy activities. Why not now?

Hypothesis 2: Business Model of the Living Dead

The most common hypothesis, which I have heard repeatedly over the past few days, views the deal as a harbinger of change for the PBM business. By selling now (at a discount), Caremark is telling us something bad about future PBM business model, despite the Q3 results posted on Thursday. However, there is no consensus on the bad news to come. (Transparency? AWP? Lawsuit? Professor Plum in the Pharmacy with a Pestle?) This hypothesis helps to explain why Caremark was recently buying back its own shares at 20%+ more than CVS is paying now.

Hypothesis 3: Over the Hedge

Some argue that Caremark is sneaking out at the top, as Matthew Holt of The Health Care Blog suggests. This hypothesis is similar to the previous one, but does not contemplate the future revelation of hidden problems. Caremark’s stock bottomed out in the late 1990’s and is up 25X since then. Future sentiment looks more negative, so perhaps it was time to trade equity in a transactional intermediary for bricks-and-mortar and a strong consumer brand. (Shades of AOL/Time Warner!) One problem with this hypothesis is the fact that the stocks have performed similarly over the past two years. (See this Yahoo!Finance chart.)

Hypothesis 4: The Santa Clause

Over the weekend, I read an intriguing analysis by The Corporate Library arguing that the merger could trigger a change of control payment to Mac Crawford (Caremark’s Chairman, President, and CEO) of $17.6 million cash and $269 million in vested equity. However, the report also indicates that a lack of disclosure makes it hard to tell what’s really going on. Caremark’s board would not allow the deal to go through just because the CEO stands to get a big payout…right?

What do you think? ‘Tis the season, so cast your vote.

A technical note on voting: This survey prevents duplicate voting from the same domain in the same day. If you see a message indicating that you already voted, it means that the survey software can’t distinguish a unique IP address from your company. Sorry, ballot stuffers!

Today’s Wall Street Journal article on Tom Ryan’s background (CVS's Deal Maker Faces Toughest Test Integrating Caremark) alludes to some of the investor discontent, noting: “Some Caremark shareholders are grumbling that the purchase price is too low; some wonder if the sale is driven by weakness in Caremark's business.” In contrast, the original article from last week (CVS, Caremark Unite to Create Drug-Sale Giant) focuses on the conflict-of-interest issues because it was co-written by Barbara Martinez.

Below are the four hypotheses that I am hearing in my conversations. Vote for your favorite (anonymously, of course). If you choose "None of the Above," please add comment to this post with your preferred explanation.

Hypothesis 1: Why not?

Given the strategic rationale for channel compression, a deal was inevitable at some point in the next few years. (My take was posted on Thursday as Consolidation of the US Pharmaceutical Infrastructure). In brief, CVS has been trying to get closer to employers and payers with Pharmacare. At the same time, Caremark has become a major dispensing pharmacy through its mail order and specialty pharmacy activities. Why not now?

Hypothesis 2: Business Model of the Living Dead

The most common hypothesis, which I have heard repeatedly over the past few days, views the deal as a harbinger of change for the PBM business. By selling now (at a discount), Caremark is telling us something bad about future PBM business model, despite the Q3 results posted on Thursday. However, there is no consensus on the bad news to come. (Transparency? AWP? Lawsuit? Professor Plum in the Pharmacy with a Pestle?) This hypothesis helps to explain why Caremark was recently buying back its own shares at 20%+ more than CVS is paying now.

Hypothesis 3: Over the Hedge

Some argue that Caremark is sneaking out at the top, as Matthew Holt of The Health Care Blog suggests. This hypothesis is similar to the previous one, but does not contemplate the future revelation of hidden problems. Caremark’s stock bottomed out in the late 1990’s and is up 25X since then. Future sentiment looks more negative, so perhaps it was time to trade equity in a transactional intermediary for bricks-and-mortar and a strong consumer brand. (Shades of AOL/Time Warner!) One problem with this hypothesis is the fact that the stocks have performed similarly over the past two years. (See this Yahoo!Finance chart.)

Hypothesis 4: The Santa Clause

Over the weekend, I read an intriguing analysis by The Corporate Library arguing that the merger could trigger a change of control payment to Mac Crawford (Caremark’s Chairman, President, and CEO) of $17.6 million cash and $269 million in vested equity. However, the report also indicates that a lack of disclosure makes it hard to tell what’s really going on. Caremark’s board would not allow the deal to go through just because the CEO stands to get a big payout…right?

What do you think? ‘Tis the season, so cast your vote.

A technical note on voting: This survey prevents duplicate voting from the same domain in the same day. If you see a message indicating that you already voted, it means that the survey software can’t distinguish a unique IP address from your company. Sorry, ballot stuffers!

Thursday, November 02, 2006

Consolidation of the US Pharmaceutical Infrastructure

Yesterday’s CVS Corp (CVS) - Caremark Rx Inc (CMX) deal led to a record traffic day here at Drug Channels as investors and the industry scrambled to make sense of the transaction. I was also pleased to help the media understand the deal. Dinah Brin of Dow Jones captured some of my thoughts in CVS, Caremark Seek Relief in Merger. I even made it into USA Today! (Thanks, Julie!)

In my view, this deal represents a logical vertical integration within the U.S. pharmaceutical infrastructure – the network of companies that facilitate dispensing and payment of pharmaceuticals. It’s also the coverage area for this blog (which I called “Drug Channels” because it had fewer letters than the “Pharmaceutical Infrastructure Blog.”)

Channel Evolution

I have been studying how channels evolve for over 15 years. The following two guiding principles, which have motivated my research and consulting in many sectors of the US economy, can help explain the current deal.

Big Unknowns

There is still much we don’t know about this deal, such as how the combined entity will work with other pharmacies to complete their retail network. See my comments in CVS/Caremark Creates Powerhouse, Unites Rivals:

But Fein adds that the fit could be awkward in other areas. In June, CVS acquired 700 Sav-On and Osco stores from Albertson's Inc. for $2.93 billion. While that helped the company solidify its national footprint, it still doesn't operate in all the markets covered by Caremark's dispensing network, which includes 60,000 retail outlets across the country. That network also includes a number of key rivals for CVS, among them Wal-Mart Stores Inc. (WMT) and Walgreen Co. (WAG).

"Strategically, Wal-Mart and Walgreen are going to have to make some tough decisions," Fein says. "I don't think they can sever their relationship with Caremark, because they need those customers. But they're going to be very nervous that Caremark could design programs that could favor CVS versus other programs.

Although the stock market doesn’t seem to love the CVS-Caremark deal, I still believe that it represents an inevitable compression of the industry.

In my view, this deal represents a logical vertical integration within the U.S. pharmaceutical infrastructure – the network of companies that facilitate dispensing and payment of pharmaceuticals. It’s also the coverage area for this blog (which I called “Drug Channels” because it had fewer letters than the “Pharmaceutical Infrastructure Blog.”)

Channel Evolution

I have been studying how channels evolve for over 15 years. The following two guiding principles, which have motivated my research and consulting in many sectors of the US economy, can help explain the current deal.

- You can remove an intermediary but not the services provided by that intermediary. I am skeptical of the “PBMs add no value” critics because it is at odds with the marketplace realities. The PBM’s success reflects many individual business decisions by payers and insurers. If PBMs really added “no value,” then sophisticated payers would simply bypass them and perform the activity themselves. There are situations where this has occurred, but there has not yet been a rush for the exits.

- The services of an intermediary eventually migrate to the lowest cost provider of those services. PBMs heritage was in transaction processing, which was at one time a valuable service. As it became commoditized, they moved on to more complex services, such as formulary design. Like all intermediaries, innovative services often become part of core expectations, so further innovation is needed or disintermediation is at hand. Matthew Holt of The Helath Care Blog suggests that Caremark is sneaking out at the top, presumably because PBMs have reached the end of the line innovation-wise. I don't agree, as evidenced by the spirited debate that he and I are having over on his blog.

The confusion and uncertainty about the transaction stems from an inherent division of labor within U.S. Drug Channels. There are three major activity sets within this infrastructure:

- Product Movement from Manufacturer to Patient

Key intermediaries: Wholesalers, Retail Pharmacies, Mail Pharmacies, Providers - Payment flow from Patients/Payers to Manufacturers

Key intermediaries: PBMs, Insurers, HMOs, Government - Product Selection from Manufacturers to Physicians

Key Intermediaries: PBMs, HMOs

Big Unknowns

There is still much we don’t know about this deal, such as how the combined entity will work with other pharmacies to complete their retail network. See my comments in CVS/Caremark Creates Powerhouse, Unites Rivals:

But Fein adds that the fit could be awkward in other areas. In June, CVS acquired 700 Sav-On and Osco stores from Albertson's Inc. for $2.93 billion. While that helped the company solidify its national footprint, it still doesn't operate in all the markets covered by Caremark's dispensing network, which includes 60,000 retail outlets across the country. That network also includes a number of key rivals for CVS, among them Wal-Mart Stores Inc. (WMT) and Walgreen Co. (WAG).

"Strategically, Wal-Mart and Walgreen are going to have to make some tough decisions," Fein says. "I don't think they can sever their relationship with Caremark, because they need those customers. But they're going to be very nervous that Caremark could design programs that could favor CVS versus other programs.

Although the stock market doesn’t seem to love the CVS-Caremark deal, I still believe that it represents an inevitable compression of the industry.

Wednesday, November 01, 2006

CVS + Caremark: I called it!

Big news this morning! CVS Corp. (CVS) and Caremark Rx Inc (CMX) are now discussing a "merger of equals." See CVS, Caremark Rx Hold Merger Talks.

But this news should not surprise faithful readers of this blog. Back on June 18, I explained the logic behind a PBM-Pharmacy Chain merger, arguing that control of the last mile in the pharmacy supply chain would lead to future chain pharmacy /PBM merger. Read my June analysis here: Walgreens' Future: I see dead canaries.

Although I was discussing Walgreens at the time, the same logic applies to a CVS-PBM combination. I wrote:

"The combined market cap of Medco, Caremark, and Express Scripts is roughly the same as Walgreens market cap. If PBM P/E ratios return to pre-2005 levels, they will be tempting targets for the retail chains."

Thanks to two unforseen events -- Wal-Mart and the AWP settlement-- valuations did drop, and look what happened!

See? This blog really can help you predict the future!

But this news should not surprise faithful readers of this blog. Back on June 18, I explained the logic behind a PBM-Pharmacy Chain merger, arguing that control of the last mile in the pharmacy supply chain would lead to future chain pharmacy /PBM merger. Read my June analysis here: Walgreens' Future: I see dead canaries.

Although I was discussing Walgreens at the time, the same logic applies to a CVS-PBM combination. I wrote:

"The combined market cap of Medco, Caremark, and Express Scripts is roughly the same as Walgreens market cap. If PBM P/E ratios return to pre-2005 levels, they will be tempting targets for the retail chains."

Thanks to two unforseen events -- Wal-Mart and the AWP settlement-- valuations did drop, and look what happened!

See? This blog really can help you predict the future!

Tuesday, October 31, 2006

Channel Conflict as Pedigree Looms

Although everyone is focused on the mid-term elections, pharmaceutical and medical products manufacturers should be paying attention to PDMA-related activity in their downstream channel.

Secondary drug wholesalers are planning to file an injunction against the FDA to stop implementation of the Prescription Drug Marketing Act (PDMA) according to this story from Drug Industry Daily. See Drug Wholesalers Seeking Injunction to Stop Drug Tracking Program.

By way of background, the FDA lifted the stay on implementation for the PDMA in June. It is now scheduled to be implemented on December 1, 2006. See my blog posts in the Pedigree category for more background on the issue as well as the FDA's Draft Compliance Policy.

Unfortunately, I have heard only limited understanding of the ADR issue in my conversations with trade relations executives at pharma companies. The FDA is apparently issuing a Q&A next week to clarify the situation. In the meantime, the filing of this injunction should serve as a channel strategy wake-up call to manufacturers that have so far ignored the December 1 PDMA implementation deadline.

----

I have to go and get ready for trick-or-treating. I'm dressing up as something very scary -- a cute, cuddly teddy bear filled with counterfeit drugs! (See Items 7 and 10.) My kids are dressing up as RFID tags. Happy Halloween!

Secondary drug wholesalers are planning to file an injunction against the FDA to stop implementation of the Prescription Drug Marketing Act (PDMA) according to this story from Drug Industry Daily. See Drug Wholesalers Seeking Injunction to Stop Drug Tracking Program.

By way of background, the FDA lifted the stay on implementation for the PDMA in June. It is now scheduled to be implemented on December 1, 2006. See my blog posts in the Pedigree category for more background on the issue as well as the FDA's Draft Compliance Policy.

I suppose that this filing was inevitable because the PDMA's Authorized Distributor of Record (ADR) system creates a powerful market dynamic toward a one-step channel. The extra costs and burdens of a two-or-more step (non-ADR) channel have the potential to shift volume among wholesale market participants. Speculatively, I imagine at least three possible outcomes from the PDMA:

- Wholesalers with an ADR relationship will pick up volume. The large wholesalers (MCK, CAH, ABC) will pick up volume from secondary drug wholesalers as well as physician distributors. Many med-surg distributors have found themselves caught between an ADR and a hard place. These companies often stock pharmaceuticals as a convenience for their physician customers but have relatively small volumes of Rx product in their mix (maybe 5% to 10% of total sales). They are not primarily secondary drug wholesalers, so need to either be ADRs or receive pedigree from a major wholesaler. For example, PSS World Medical issued a press release announcing its intent to buy directly from manufacturers after HB371 passed in Florida. (See PSS' Press Release.)

- Manufacturers will broaden their ADR networks. Contrary to popular belief, most pharma companies have authorized distributors beyond the big 3. The top eight manufacturers average of 79 ADRs according to published lists that I reviewed over the summer.

- The marketplace will create a solution for pedigree. A third option would be to allow the marketplace to determine winners and losers. If customers truly demand to purchase from a secondary wholesaler, then we can expect manufacturers to require ADRs to service those wholesalers. A manufacturer could even compensate an ADR for fulfillment to secondary distributors, making ADRs into de facto master wholesalers and possibly creating another area of fee-for-service compensation for wholesalers.

Unfortunately, I have heard only limited understanding of the ADR issue in my conversations with trade relations executives at pharma companies. The FDA is apparently issuing a Q&A next week to clarify the situation. In the meantime, the filing of this injunction should serve as a channel strategy wake-up call to manufacturers that have so far ignored the December 1 PDMA implementation deadline.

----

I have to go and get ready for trick-or-treating. I'm dressing up as something very scary -- a cute, cuddly teddy bear filled with counterfeit drugs! (See Items 7 and 10.) My kids are dressing up as RFID tags. Happy Halloween!

Thursday, October 26, 2006

Additional Comments on the AWP settlement

A number of people have asked me to follow-up on my AWP Ain’t What Matters post with additional comments on the proposed First DataBank AWP settlement. This post provides a few high-level observations but will refrain from a thorough explanation of potential implications.

The $4 Billion Man

The October 6 Wall Street Journal article highlighted a $4 billion per year savings estimate. Anyone interested in this matter should spend some time reading through the underlying report to understand the assumptions behind the headline. (See Impact and Cost Savings of the First DataBank Settlement Agreement.)

In theory, a one-time adjustment to AWP will have a minimal impact as long as contracts can be renegotiated to preserve the original dollar-cost economic arrangements. So pay particular attention to footnote 19 on page 6, which provides Dr. Hartman’s reasons for believing that market participants will not be able to easily reverse the effect of the settlement with renegotiations.

Hartman’s viewpoints contrast with certain public statements, such as CVS’ press release: “In the event AWPs were suddenly reduced in a material way for particular products, obviously we would renegotiate the discount or dispensing fee. Virtually all of our commercial agreements are 'at-will' agreements, which can be renegotiated freely.” (See CVS Corporation Statement Regarding AWP.) Express Scripts was much more circumspect in its 10-Q filing this week, which created this week’s share price volatility.

Look Back in Anger?

We also don’t know the extent of look-back lawsuits against retail pharmacies by entities that are not part of the settlement class.

In reading the First DataBank court documents, I was struck by the fact that the First DataBank AWP settlement excludes all state and federal government payers from the settlement class. But 49 states use “discount from AWP” to compute Estimated Acquisition Cost (EAC) as the basis for pharmacy ingredient reimbursement under Medicaid. The median discount is 12% (range: -5% to -50%). Seven states have generic-specific formulas ranging from -20% to -50%.

Inflated AWP values would have also inflated Medicaid ingredient reimbursements to retail and mail pharmacies. Note that Medicaid rebates from manufacturers to the states are not affected because these rebates are computed based on Average Manufacturer Price and Best Price data.

On one hand, CVS’ comments on the relationship between negotiated discounts and AWP is consistent with the observation that we didn’t see windfall profits for pharmacy chains and PBM mail order in 2002. But reimbursement discounts did not widen for Medicaid EAC calculations. Will states make additional claims against retail pharmacies for Medicaid payments? Does this create financial/legal liability for the retail pharmacy industry?

And here’s a real brain-twister: How does the settlement affect the projected savings from the 2005 Deficit Reduction Act’s switch from AWP to AMP-based formulas? NACDS’ position paper notes that DRA switch reduces payments to community retail pharmacy by $6.3 billion over the next 5 years. (See Implications of Federal Medicaid Generic Drug Payment Reductions For State Policymakers.) If you believe Dr. Hartman’s analyses, about $2.5 billion of these savings will never materialize.

Looks like we’ll be living with the AWP settlement for a long time.

The $4 Billion Man

The October 6 Wall Street Journal article highlighted a $4 billion per year savings estimate. Anyone interested in this matter should spend some time reading through the underlying report to understand the assumptions behind the headline. (See Impact and Cost Savings of the First DataBank Settlement Agreement.)

In theory, a one-time adjustment to AWP will have a minimal impact as long as contracts can be renegotiated to preserve the original dollar-cost economic arrangements. So pay particular attention to footnote 19 on page 6, which provides Dr. Hartman’s reasons for believing that market participants will not be able to easily reverse the effect of the settlement with renegotiations.

Hartman’s viewpoints contrast with certain public statements, such as CVS’ press release: “In the event AWPs were suddenly reduced in a material way for particular products, obviously we would renegotiate the discount or dispensing fee. Virtually all of our commercial agreements are 'at-will' agreements, which can be renegotiated freely.” (See CVS Corporation Statement Regarding AWP.) Express Scripts was much more circumspect in its 10-Q filing this week, which created this week’s share price volatility.

Look Back in Anger?

We also don’t know the extent of look-back lawsuits against retail pharmacies by entities that are not part of the settlement class.