Drug Channels delivers timely analysis and provocative opinions from Adam J. Fein, Ph.D., the country's foremost expert on pharmaceutical economics and the drug distribution system. Drug Channels reaches an engaged, loyal and growing audience of more than 100,000 subscribers and followers. Learn more...

Showing posts with label Mergers and Acquisitions. Show all posts

Showing posts with label Mergers and Acquisitions. Show all posts

Don't forget to register for DCI’s next webinar on Friday, April 10, 2026, from 12:00 p.m. to 1:30 p.m. ET. Adam J. Fein and Bryce Platt will unpack the good, the bad, and the ugly of the PBM industry—and explore what it means for you. Click here to learn more and sign up.

In recent years, these companies have spent more than $16 billion to acquire management service organizations (MSOs) that oversee physician practices in such specialties as gastroenterology, oncology, ophthalmology, and urology.

Below, we highlight the largest MSO transactions and explore five ways wholesalers benefit from ownership in their downstream physician customers. Ultimately, these strategies may allow wholesalers to exert unprecedented control over market access for provider-administered drugs—if they can figure out how to realize this power.

In recent years, these companies have spent more than $16 billion to acquire management service organizations (MSOs) that oversee physician practices in such specialties as gastroenterology, oncology, ophthalmology, and urology.

Below, we highlight the largest MSO transactions and explore five ways wholesalers benefit from ownership in their downstream physician customers. Ultimately, these strategies may allow wholesalers to exert unprecedented control over market access for provider-administered drugs—if they can figure out how to realize this power.

Special launch pricing is available through October 27, 2025.

This report—our sixteenth edition—remains the most comprehensive, data-driven resource for understanding and analyzing the large and growing U.S. pharmaceutical distribution industry.

With 9 chapters, more than 400 pages, 187 exhibits, and over 850 endnotes, this report is unmatched in scope and depth. There’s simply no other resource like it.

Order today to secure your copy of this fully updated, revised, and expanded 2025-26 edition at special discounted prices.

The 2025-26 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors remains the most comprehensive, fact-based tool for understanding and analyzing the large and growing U.S. pharmaceutical distribution industry. Widely regarded as the industry standard, this encyclopedic resource offers a definitive guide to wholesale distribution’s role in the complex web of U.S. prescription drug channels.

The chart below illustrates the vertical integration and broad reach of the three largest companies in U.S. pharmaceutical distribution. The numbers in the chart correspond to the report chapter that explains and analyzes the specific business segment.

Updated analyses of strategies, market positions, and executive compensation for the Big Three—Cencora, Cardinal Health, and McKesson. We review each company’s business segments and underlying business profitability, based upon our proprietary economic models. This allows you to assess differences among the public companies’ organizational structure and financial performance.

Self-contained chapters that do not need to be read in order. (Really!) There are loads of internal hyperlinks to help you navigate the document and customize it to your specific interests and priorities.

The option to download an additional PowerPoint file with images of all 178 exhibits. This popular option helps you share the insights and data with others in your organization. (The exhibits appear within the text for all license versions.)

760 (!) endnotes, most of which have direct hyperlinks to original source materials for deeper learning.

No SpongeBob Squarepants, corny jokes, or pop culture references, all of which have been reluctantly removed.

Thank you for your continued interest in our research. Please email me (afein@drugchannels.net) with any questions before purchasing.

We look forward to sharing this year’s insights with you.

With 9 chapters, 400+ pages, 187 exhibits, and 850+ endnotes, this report is unmatched in scope and depth. There is no other resource like it.

Preorder today to secure this fully updated, revised, and expanded 2025-26 edition at special discounted prices. Preorders ensure early access. You’ll receive the report before its October 14 release date.

Special preorder and launch pricing discounts will be valid through October 27, 2025. Act now to maximize savings.

The chart below highlights the three largest companies’ vertical alignment and diverse roles within the U.S. healthcare system. The numbers in the chart indicate the report chapter that corresponds to, explains, and analyzes each business.

[Click to Enlarge]

The 2025-26 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors remains the most comprehensive, fact-based tool for understanding and analyzing the large and growing U.S. pharmaceutical distribution industry. Widely regarded as the industry standard, this encyclopedic resource offers a definitive guide to wholesale distribution’s role in the complex web of U.S. prescription drug channels.

Our 2025-26 edition contains the most current financial and industry data about the distribution of pharmaceuticals and the major companies that handle these products. As always, we have updated all market and industry data with the most current information available. The report also updates our annual analyses of the strategies, market positions, and executive compensation of the three largest companies: Cencora, Cardinal Health, and McKesson.

We review each wholesaler’s business segments and underlying business profitability, based upon our proprietary economic models. This information allows you to assess differences among the public wholesalers’ business organizations, strategies, and financial performance. Where appropriate, financial data have been restated based on updated disclosures.

Thank you for your continued interest in our research. Please email me (afein@drugchannels.net) with any questions before purchasing. We look forward to sharing this year’s insights with you.

Our news-laden summer is ending. Time to pack away your bathing suit, send the kids back to school, and cherish these curated curiosities that I combed from the Drug Channels coastline:

This week, I’m rerunning some popular posts while I prepare for tomorrow's live video webinar: What’s Next for Retail Pharmacy: Data, Debate, and Disruption. I’ll be joined by special guest Antonio Ciaccia, CEO of 46brooklyn Research, and President of 3 Axis Advisors.

It's time for Drug Channels’ annual update of vertical integration among insurers, PBMs, specialty pharmacies, and healthcare services within U.S. drug channels. As you can see below, we have revised, renovated, and refurbished our infamous illustration of the major vertical business relationships among the largest companies.

Proponents of these vertical integration arrangements argue that they create opportunities to mine healthcare costs. However, these organizations remain highly controversial, due to the potential for anti-competitive behavior. We summarize some of the key issues below.

While some major companies have narrowed their focus or unwound previous integration efforts, ongoing consolidation and selective deconsolidation will continue to reshape the healthcare biome by trying to build something epic, block by block.

It's time for Drug Channels’ annual update of vertical integration among insurers, PBMs, specialty pharmacies, and healthcare services within U.S. drug channels. As you can see below, we have revised, renovated, and refurbished our infamous illustration of the major vertical business relationships among the largest companies.

Proponents of these vertical integration arrangements argue that they create opportunities to mine healthcare costs. However, these organizations remain highly controversial, due to the potential for anti-competitive behavior. We summarize some of the key issues below.

While some major companies have narrowed their focus or unwound previous integration efforts, ongoing consolidation and selective deconsolidation will continue to reshape the healthcare biome by trying to build something epic, block by block.

ICYMI, the largest three pharmaceutical wholesalers—Cardinal Health, Cencora, and McKesson—are using vertical integration to build significant market positions in businesses beyond drug distribution.

In the video clip below, I review the vertical integration status of the largest three pharmaceutical wholesalers, illustrated in the chart below.

[Click to Enlarge]

I also:

Explain how wholesalers have strengthened their position in buy-and-bill channels for provider-administered drugs through vertical integration with their downstream customers.

Discuss how and why private equity roll-up activity has provided wholesalers with strategic opportunities to acquire ownership stakes in practice management companies.

Outline the market access implications for provider-administered biosimilars in the buy-and-bill market.

Three’s still company in the world of pharmacy benefit managers.

For 2024, nearly 80% of all equivalent prescription claims were processed by three familiar companies: the CVS Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group. The names haven’t changed, but shifting relationships and contract shakeups have altered the plot, with Express Scripts stepping into a new lead role.

Below, we break down the latest market share data from Drug Channels Institute (DCI), explore the developments driving these changes, and examine what they signal for the future of the PBM landscape.

ICYMI, the largest three pharmaceutical wholesalers—Cardinal Health, Cencora, and McKesson—are using vertical integration to build significant market positions in businesses beyond drug distribution.

In the video clip below, I review the vertical integration status of the largest three pharmaceutical wholesalers, illustrated in the chart below.

[Click to Enlarge]

I also:

Explain how wholesalers have strengthened their position in buy-and-bill channels for provider-administered drugs through vertical integration with their downstream customers.

Discuss how and why private equity roll-up activity has provided wholesalers with strategic opportunities to acquire ownership stakes in practice management companies.

Outline the market access implications for provider-administered biosimilars in the buy-and-bill market.

As regular readers of Drug Channels know, U.S. distribution and dispensing channels for prescription drugs are undergoing significant evolution and consolidation as the changing economics of pharmaceuticals challenge conventional business models.

During this period of volatility, the core business model of the Big Three public pharmaceutical distribution companies—Cardinal Health, Cencora, and McKesson—remains intact. Put simply: Buy low, sell high, collect early, and pay late.

But as I explain below, wholesalers continue to position themselves as essential intermediaries by expanding their industry position and strengthening their economic fundamentals.

Read on for five key pricing, pharmacy, provider, and manufacturer trends that are driving the U.S. drug wholesaling industry.

Three is still the magic number for pharmacy benefit managers (PBMs).

For 2023, nearly 80% of all equivalent prescription claims were processed by three companies: the Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group.

Read on for Drug Channels Institute’s (DCI’s) latest market share figures, along with a preview of the industry changes that will shift these shares over the next few years.

It's time for Drug Channels’ annual update of vertical integration among insurers, PBMs, specialty pharmacies, and providers within U.S. drug channels.

Below you’ll find our latest illustration of the major vertical business relationships among the largest companies along with some of the notable activity since our previous update. These organizations continue to exert greater control over patient access, sites of care/dispensing, and pricing, although some have started to unwind their vertical efforts.

The companies face renewed scrutiny from the Federal Trade Commission, the Office of Inspector General, and members of Congress. But until anyone takes action, we will continue to live with the golden rule of the drug channel: Whoever has the gold gets to make the rules.

Three is still the magic number for pharmacy benefit managers (PBMs).

For 2023, nearly 80% of all equivalent prescription claims were processed by three companies: the Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group.

Read on for Drug Channels Institute’s (DCI’s) latest market share figures, along with a preview of the industry changes that will shift these shares over the next few years.

It’s finally spring in Philadelphia, home of Drug Channels. Along with sunshine and fine weather, the vernal equinox has ushered in a crop of new and noteworthy stories:

What the CarelonRx/Kroger specialty pharmacy deal means for CVS Health

Provider-owned specialty pharmacies expand in Medicare

Payers are not keen on shady alternative funding programs (AFP)

Hospitals’ association spreads 340B misinformation

In case you haven’t noticed, private equity firms have displaced hospitals and health systems as the major acquirers of community oncology practices. These financial firms have assembled significant oncology practice management companies that are primed for purchase by drug channel participants.

Below, I review recent M&A trends and then examine the strategic objectives behind the acquisition of private-equity-backed OneOncology by AmerisourceBergen (Cencora) and another financial buyer. As I explain, AmerisourceBergen (Cencora) gains significant strategic advantage from this transaction, which echoes a historical McKesson deal.

The Federal Trade Commission’s (FTC) has a newfound interest in the roll-up transactions that are creating practice management companies. Nonetheless, I expect this consolidation activity to continue—enabling a new round of vertical integration in the drug channel.

In case you haven’t noticed, private equity firms have displaced hospitals and health systems as the major acquirers of community oncology practices. These financial firms have assembled significant oncology practice management companies that are primed for purchase by drug channel participants.

Below, I review recent M&A trends and then examine the strategic objectives behind the acquisition of private-equity-backed OneOncology by AmerisourceBergen (Cencora) and another financial buyer. As I explain, AmerisourceBergen (Cencora) gains significant strategic advantage from this transaction, which echoes a historical McKesson deal.

The Federal Trade Commission’s (FTC) has a newfound interest in the roll-up transactions that are creating practice management companies. Nonetheless, I expect this consolidation activity to continue—enabling a new round of vertical integration in the drug channel.

Yesterday’s reflections on Asembia’s Specialty Pharmacy Summit included a link to the general session slides. My portion of the deck included an updated mapping of vertical integration among insurers, PBMs, specialty pharmacies, and providers within U.S. drug channels. Many readers asked for a standalone version of this infamous chart.

So, for your viewing and slide making pleasure, below you’ll find my latest illustration of the major vertical business relationships among the largest companies.

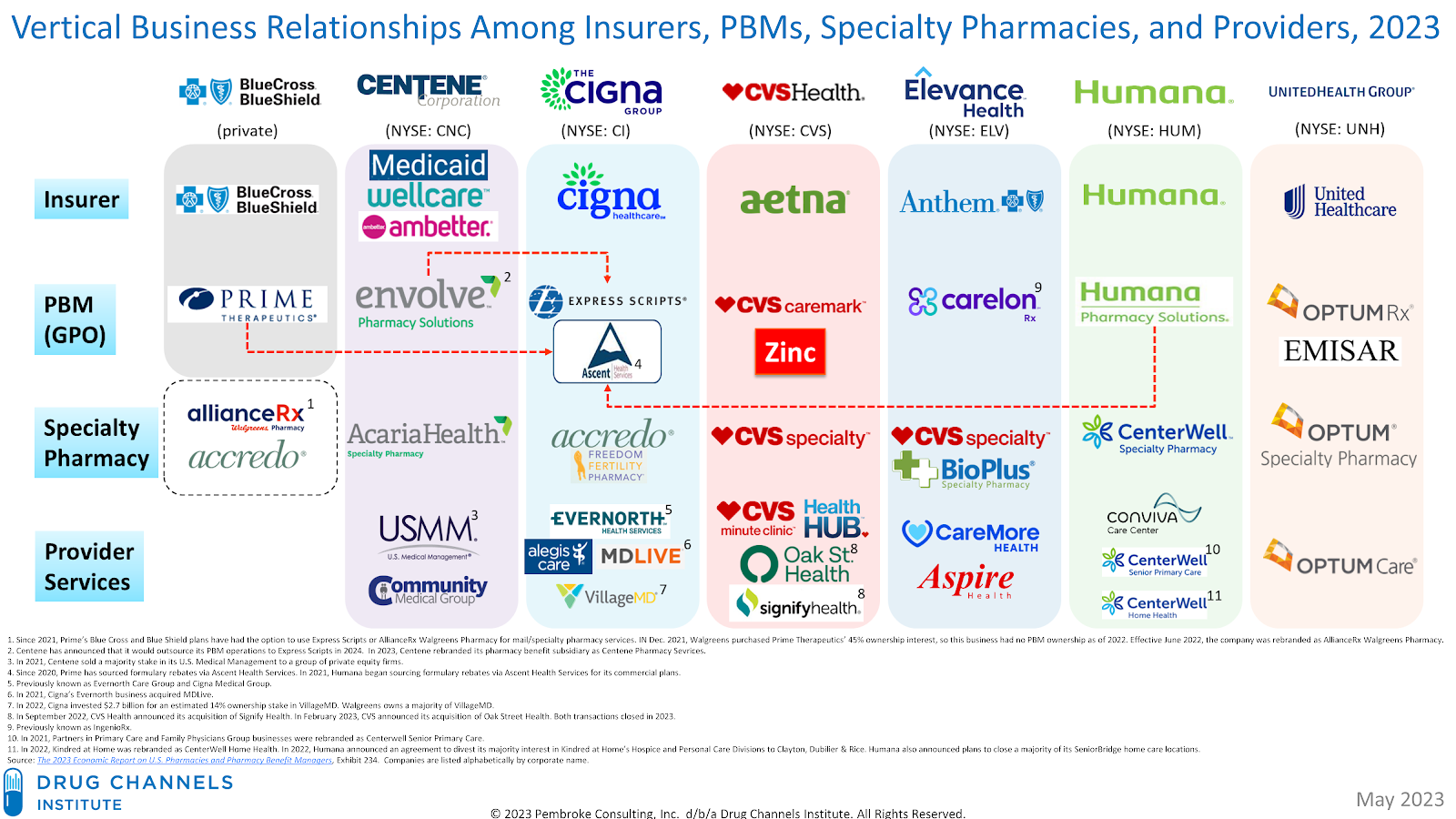

I estimate that at least half of all public and private U.S. healthcare spending flows through these seven familiar entities: Blue Cross Blue Shield, Centene, Cigna, CVS Health, Elevance Health, Humana, and United Health Group. Just like the heroes in Dawn of the Seven, they are here to serve and protect you.

Consolidation has brought together large, economically significant insurer/PBM/specialty pharmacy/provider organizations within U.S. drug channels. At least half of all U.S. healthcare spending flows through these seven familiar entities: Blue Cross Blue Shield, Centene, Cigna, CVS Health, Elevance Health, Humana, and United Health Group.

In the brief video clip below, I review these businesses and offer some thoughts on their positioning for 2023. As you’ll see, the vertical strategy shakeout is underway.

This week, I’m rerunning some popular posts while I prepare for tomorrow's live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow's live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar:

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar: