As you will see below, outpatient prescription drugs dispensed by retail and mail pharmacies are projected to remain a small share (8.4%) of total U.S. healthcare spending. What’s more, taxpayers—via Medicare and Medicaid—will continue to crowd out the private insurance market. One bright spot: consumers will account for an ever-smaller share of drug spending.

Thus, the government actuaries expect that pharmaceuticals will not be the key driver of U.S. healthcare spending growth. Will someone tell our elected officials?

I ♥ DATASpeaking of prescription drug payment, be sure to sign up for my new live video webinar, PBM Industry Update: Trends, Controversies, and Outlook, on April 22, 2022, from 12:00 p.m. to 1:30 p.m. ET.

The Office of the Actuary at CMS publishes projections for U.S. National Health Expenditures (NHE). These projections include spending on prescription drugs sold through outpatient retail, mail, and specialty pharmacies.

It’s been more than two years since CMS last issued spending projections. Unfortunately, the COVID-19 pandemic immediately made the March 2020 predictions obsolete. I reviewed them anyway in April 2020.

As always, I encourage you to review the source materials:

- Health Affairs article: National Health Expenditure Projections, 2021–30: Growth To Moderate As COVID-19 Impacts Wane (The article is free for subscribers; others may purchase it.)

- National Health Expenditure Projections And A Few Ways We Might Avoid Our Fate (Commentary from Michael Chernew, chair of the Medicare Payment Advisory Commission)

- National Health Expenditures data files (Party time!)

See the NOTES FOR NERDS section at the bottom of this post for some important details.

NOT PROJECTED TO SKYROCKET

The top line projections highlight the government’s official, apolitical view that prescription drugs will have a modest impact on U.S. healthcare costs.

Outpatient prescription drug spending from retail and mail pharmacies is expected to grow at a rate comparable to overall healthcare spending. CMS projects that from 2020 to 2030, total health spending will grow at an average rate of 5.1%, while prescription drug spending will at an average rate of 5.0%.

Consequently, outpatient prescription drug spending is projected to remain a small and stable portion of overall U.S. healthcare expenditures. CMS projects that outpatient prescription drugs will account for 8.4% of 2030 national healthcare expenditures—compared with 8.4% in 2020.

Long-time NHE fans know that CMS’ projections of drug spending growth have, on average, overestimated this spending, so the figures could be even lower. See Chart #3 in the Analysis of National Health Expenditure Projections Accuracy for some commentary on the factors behind these historical underforecasts.

QUE SERÁ, SERÁ

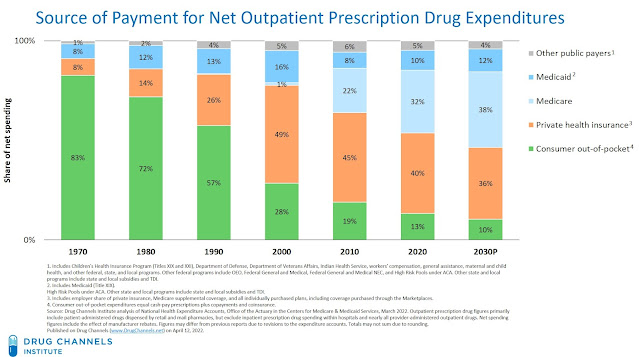

The chart below presents our summary of the historical and projected payer mix for net prescription spending.

[Click to Enlarge]

Observations on these projections:

- Medicare and Medicaid will continue to crowd out other payers of prescription drugs. Medicare’s share of overall prescription spending increased from 2% in 2005 to 18% in 2006, when the Part D program launched. It has since grown to the 32% shown above. Over the past 15 years, Medicaid has been the fastest-growing source of insurance coverage in the U.S. For more on Medicaid’s growth, see Section 4.1.1. of our new 2022 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers.

CMS has assumed that as the U.S. population ages, the employer-sponsored insurance market will continue to shrink, while Medicare will grow. From 2020 to 2030, Medicare’s net spending on prescription drugs will grow at an average annual rate of 7%, while Medicaid will grow by 6.6% per year. Despite generally having the lowest net drug prices, Medicaid’s share of prescription drug spending is also projected to grow. Consequently, their collective share of net spending will grow by eight percentage points, to 50%.

Including other state and federal programs, CMS projects that public funds will account for more than half of outpatient retail prescription spending from 2025 onward.

- The commercial market will grow more slowly than public payers. Private health insurance for prescription drugs grew most quickly during the 1980s and 1990s, as most employers began adding pharmacy benefits. Its share peaked in 2001, at 50% of net prescription drug spending. Private insurance paid for only 40% of outpatient drug spending in 2020.

CMS projects that private health insurance spending on prescription drugs will grow at an average annual rate of 3.8% from 2020 to 2030. That’s slower than other payers, so private insurance’s share will drop to 36%.

- Consumers’ share of outpatient drug spending will continue to decline, but remain disproportionately higher than that of other healthcare services. In 2020, consumers’ out-of-pocket prescription expenses—cash-pay prescriptions plus copayments and coinsurance—were $46.5 billion. That equated to 13% of net outpatient prescription drug expenditures. As you can see from the chart above, consumers’ collective share of outpatient prescription drug expenditures has declined over time. Consumer expenses accounted for 83% of total U.S. outpatient prescription drug expenditures in 1970. CMS projects that consumers’ share will continue to decline, to 10% of net spending by 2030.

As I noted in my review of the 2020 historical data, consumers shoulder a much higher portion of drug spending compared with their share of hospital spending. For 2030, CMS projects that consumers’ out-of-pocket spending for hospital care will be $59.8 billion—comparable to consumer’s projected $59.1 billion out-of-pocket spending for outpatient prescriptions. However, hospital spending is projected to reach $2.2 trillion by 2030, while outpatient drug spending is projected to hit $567 billion.

Prediction is very difficult, especially if it's about the future. But everyone in the drug channel should expect that the government’s behind-the-scenes influence will be even greater in the coming years than it is today.

This doesn’t mean that we are headed for a government-run healthcare system. Instead, I expect that most of the government’s spending will continue to be managed by private companies, via Medicare Part D prescription drug plans, Medicare Advantage, managed Medicaid, and private insurance purchased on the public exchanges.

Like it or not, the vertically integrated insurer/PBM/specialty pharmacy/provider mega-organizations will become even more powerful in U.S. drug channels.

NOTES FOR NERDS

- U.S. drug spending in the NHE is roughly equivalent to total retail, mail, long-term care, and specialty pharmacies’ prescription revenues minus manufacturer rebates to third-party payers. It therefore differs from pharmacies’ prescription revenues, manufacturers’ revenues, and the “invoice price spending” purchasing data reported by IQVIA.

- The NHE’s outpatient drug spending data do not measure total U.S. spending on prescription drugs. That’s because inpatient prescription drug spending within hospitals and spending on nearly all provider-administered outpatient drugs are reported within the hospital and professional services categories. CMS does not break out these figures, but Altarum has estimated that provider-administered drugs account for additional drug expenditures of 4% to 5% of NHE.

- The NHE’s Medicare figures combine Part D drug expenditures with a small amount of Part B spending in traditional Medicare fee-for-service programs. Its private health insurance figures include employer-sponsored insurance, Medicare supplemental coverage, and all individually purchased plans, including coverage purchased through the Marketplaces.

- The NHE’s projections provide less detail than the historical data set from 2020. In Chapter 4 of our new 2022 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers, I use this detail to provide separate spending estimates of employer-sponsored vs. individually purchased private insurance.

No comments:

Post a Comment