In recent years, each of these companies has launched new group purchasing organizations (GPOs) to further consolidate the number of covered lives in rebate negotiations with pharmaceutical manufacturers. Today, I examine these PBM-owned GPOs and then speculate on five plausible explanations for their existence. I also highlight a sixth, alleged rationale that is currently the subject of litigation.

The Federal Trade Commission (FTC) has recently started investigating these GPOs. I wonder if this additional focus will deepen the FTC’s ongoing investigation—or slow it down even further?

For more on PBMs, sign up for my new live video webinar, PBMs and the Battle Over Patient Support Funds: Accumulators, Maximizers, and Alternative Funding, on June 23, 2023, from 12:00 p.m. to 1:30 p.m. ET. Click here to learn more and register.

Today’s post is adapted from Section 5.2.4. of our 2023 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers.

MEET THE NEW BOSSES

In recent years, the largest PBMs have launched new group purchasing organizations (GPOs) that handle certain rebate negotiations with manufacturers and provide other services to manufacturers and the groups’ members. To date, these groups are focused on commercial, nongovernmental business.

By aggregating the purchasing volume of its members, a GPO lowers its members’ cost of goods and reduces in-house contracting functions. Generally, a GPO does not directly purchase from suppliers or take physical possession of goods. Instead, it arranges contracts between its members and pharmaceutical manufacturers, and provides various fee-based services for manufacturers. GPOs are common for such provider groups as hospitals and physician practices.

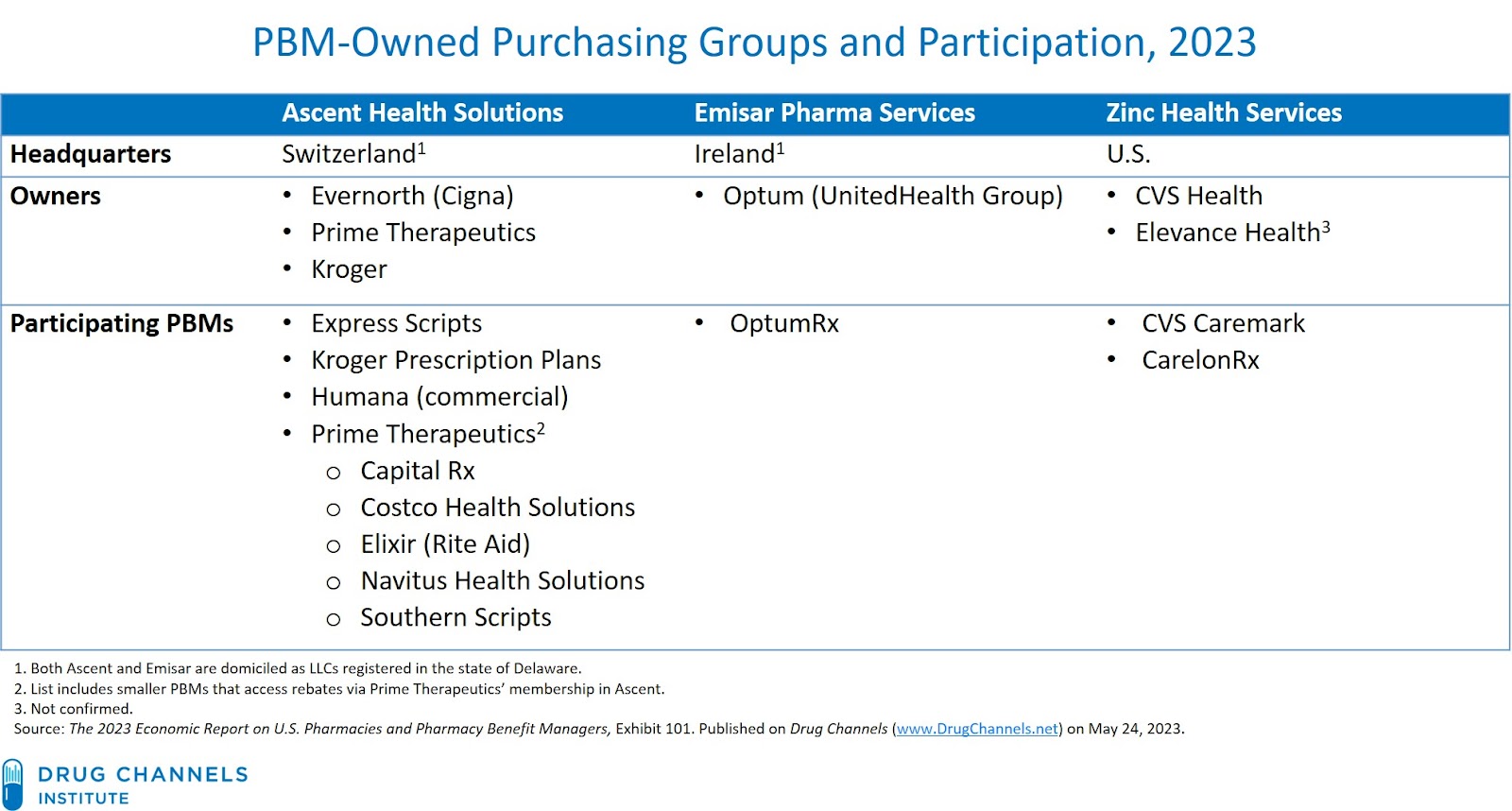

Here are brief profiles of the three major PBM-owned GPOs:

- Ascent Health Services is a Switzerland-based group purchasing organization formed in 2019. Ascent is domiciled as an LLC in Delaware.

This organization is part of Cigna’s Evernorth segment, although Kroger and Prime Therapeutics also hold ownership stakes in the business. Ascent now handles certain rebate negotiations for Express Scripts’ PBM business, Prime Therapeutics, and Kroger Prescription Plans, the small PBM owned by Kroger.

In April 2021, Humana began sourcing formulary rebates for its commercial health plans via Ascent Health Services. Humana’s fully insured commercial and administrative services only (ASO) medical membership accounts for less than 10% of its medical membership as of December 31, 2022. Note that Humana recently announced that it will be exiting the employer commercial medical insurance business.

Multiple smaller PBMs also source rebates via Prime Therapeutics. Publicly-disclosed examples include Capital Rx, Costco Health Solutions, Rite Aid’s Elixir business, Magellan Rx (now part of Prime), Navitus Health Solutions, and Southern Scripts.

A couple of years ago, Express Scripts’ PR team told me in no uncertain terms: “Ascent is not a GPO.” The company has since changed its tune, judging by this page on its new The Facts about Express Scripts website.

- Emisar Pharma Services is a GPO that is part of UnitedHealth Group’s Optum business. It launched in 2021 and began contracting for the 2022 plan year. I believe that Emisar’s primary operations are in Ireland. Like Ascent, it is domiciled as an LLC in Delaware.

In addition to Emisar, UnitedHealth Group also operates the Coalition for Advanced Pharmacy Services (CAPS), a separate rebate aggregator.

- Zinc Health Services is a U.S.-based contracting entity formed in 2020 by CVS Health. Elevance Health reportedly owns a minority interest in Zinc, although this has not been confirmed by CVS.

[Click to Enlarge]

BUT WHY?

Here are my five plausible explanations behind the creation of these new purchasing entities:

1. Provide contracting and rebate negotiation services for the combined formulary volume of multiple PBMs.

A multi-PBM organization enables the groups to gain access to more competitive rebate arrangements. However, each group member can structure their own contracts and arrangements with their respective plan sponsor clients.

2. Develop new revenue sources from manufacturers.

The PBMs’ GPOs are paid by pharmaceutical manufacturers. These payments may come from contracting entity administrative fees, prescription data services, data portals, enterprise fees, and other sources. These revenues are earned in addition to the PBMs’ typical administrative service fees, which average 3% to 5% of the WAC list price value of a drug.

Consequently, revenues from manufacturers have become crucial to PBMs’ profitability. (See Section 11.2.3. of our 2023 pharmacy/PBM report.)

Consequently, revenues from manufacturers have become crucial to PBMs’ profitability. (See Section 11.2.3. of our 2023 pharmacy/PBM report.)

3. Generate revenues and fees that may not be fully shared with the PBMs’ plan sponsor clients.

PBM compensation models are shifting, due to increased scrutiny by payers, regulators, and politicians. Plan sponsors are more sophisticated and seek greater pass-through of rebates, admin fees, and other manufacturer-provided revenues. The GPOs businesses and finances are less transparent to plan sponsors, so we estimate that a smaller share of those revenues are passed through to plan sponsors.

4. Permit tax efficiencies due to transfer pricing and rebate accounting using other countries’ lower corporate tax rates.

This rationale only applies to the GPOs located outside the United States.

5. Provide PBMs with a hedge against potential reform of PBM pricing practices.

For example, various regulatory and legislative changes could prohibit various sources of PBMs’ current profitability. These include rebate reform, bans on spread pricing, limits on copay accumulators and maximizers, changes to the 340B Drug Pricing Program, and more. However, there is no parallel effort to alter GPO safe harbor rules. Today, GPOs are compensated via manufacturer-paid administrative and service fees that are typically computed as a percentage of the purchase price that the healthcare provider pays for a product bought through a GPO contract.

Ohio Attorney General Dave Yost has alleged another, more nefarious rationale for the emergence of PBM-owned GPOs. His new lawsuit alleges that Cigna, Humana, and Prime Therapeutics shared "pricing and other information" gathered by the Ascent Health Services GPO "to gain leverage during negotiations with drugmakers for rebates." Click here to read the full complaint. Friendly reminder: A legal complaint includes only the plaintiff's allegations, so the defendants should be presumed innocent.

TL;DR

The GPOs provide a novel way for PBMs to extract incremental fees from drug makers while creating a non-rebate flow of funds for themselves—while adding more air to the gross-to-net bubble.

After all, inserting another intermediary into the drug channel always adds transparency. Right?

No comments:

Post a Comment