One is my chart showing the key channel flows within the entire U.S. pharmaceutical distribution, payment, and reimbursement system.

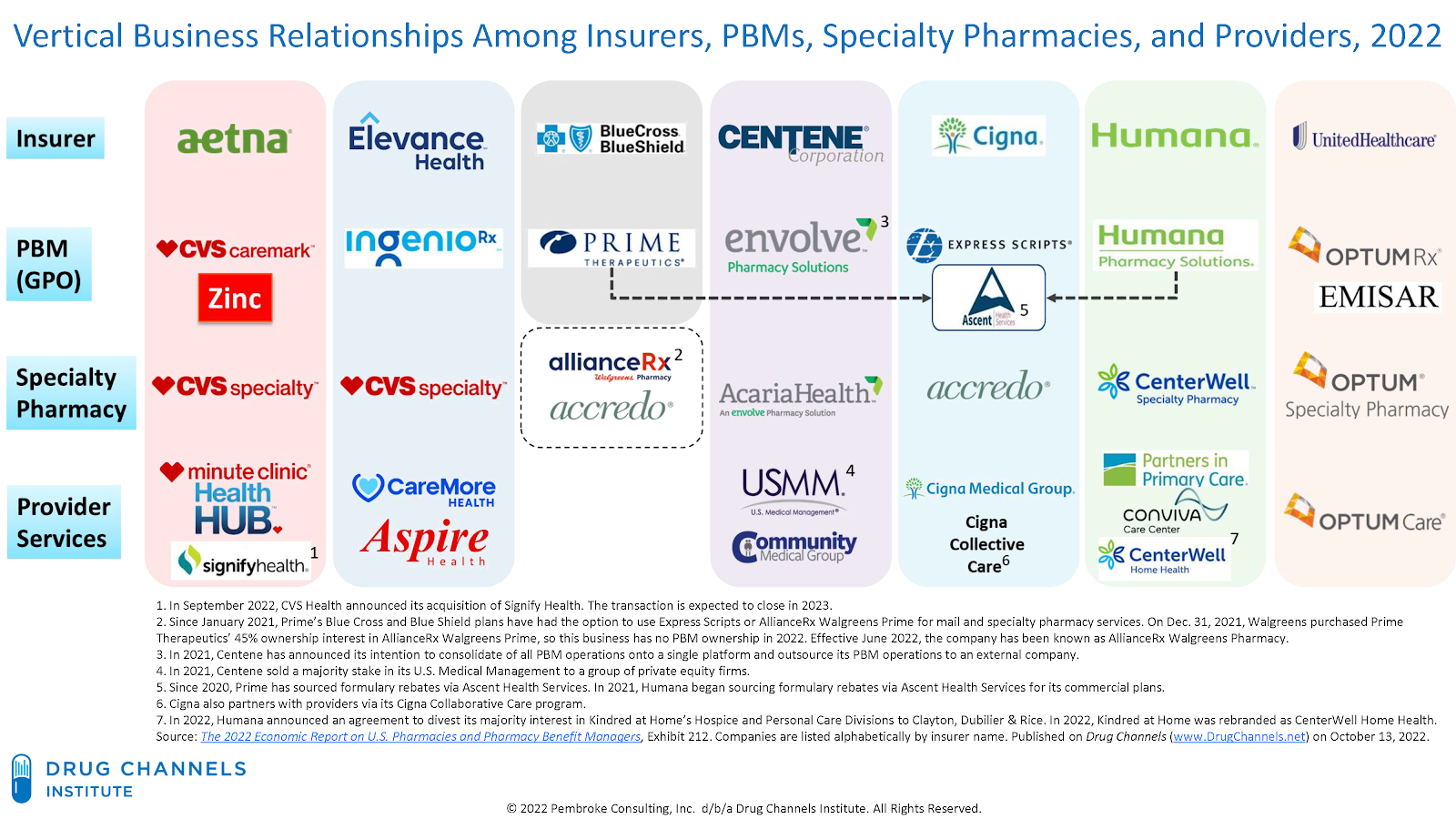

The other is my mapping of the insurer/PBM/specialty pharmacy/provider organizations that now dominate U.S. drug channels. Below, I provide an updated version of this second chart that reflects some recent transactions and name changes. About half of all U.S. healthcare spending flows through the seven companies shown below.

These organizations are poised to exert greater control over patient access, sites of care/dispensing, and pricing. But as I note below, Federal Trade Commission chair Lina M. Khan has other ideas about these companies.

THE MUNIFICENT SEVEN

The chart below provides an updated illustration of the major vertical business relationships among the largest companies in the U.S. healthcare system. The companies are listed alphabetically by the name of the insurer. An earlier version of this chart appears as Exhibit 212 in our 2022 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers.

[Click to Enlarge]

Various transactions have combined companies that offer health insurance with PBMs that operate specialty pharmacies. These include CVS Health’s acquisition of Aetna, Cigna’s acquisition of Express Scripts, Anthem’s formation of IngenioRx (and relationship with CVS Health), and the multifaceted partnerships between Express Scripts and Prime Therapeutics.

For more background on these companies’ market positions, check out three of our most popular analyses: Notably, some of these companies have begun to unwind their vertical integration efforts:

- Prime Therapeutics sold its interest in the AllianceRx Walgreens Prime mail and specialty pharmacy business. (The business is now wholly-owned by Walgreens Boots Alliance and is known as AllianceRx Walgreens Pharmacy.) Beginning in 2020, Express Scripts took over retail pharmacy network contracting for a majority of Prime’s business. Prime also began sourcing a portion of its commercial rebates via Evernorth’s Ascent Health Services.

- In 2021, Centene sold a majority stake in its U.S. Medical Management to a group of private equity firms. During 2022, the company has divested PANTHERx to three private equity firms and announced the sale of Magellan Health’s Magellan Rx PBM to Prime Therapeutics.

Centene plans to outsource its PBM operations to an external company. Last April, it issued an RFP for a 2024 PBM contract. The transaction may or may not include Centene’s remaining specialty pharmacy businesses.

Federal Trade Commission Chair Lina M. Khan has signaled serious concerns about the extent of vertical integration shown above. Here’s what she said in a June 2022 speech:

“It was policy choices that permitted PBMs to merge with one another, creating a more concentrated market. It was policy choices that permitted PBMs to vertically merge with health insurance companies on one side and specialty and retail pharmacies on the other side, which many have noted can create a sharp conflict of interest. It was policy choices that allowed the largest insurance companies and hospitals and private equity companies to buy up thousands of physician practices, which many have claimed has degraded patient care. And it was policy choices that have created a situation where Americans pay tens of billions of dollars for prescription drugs that were originally researched and developed with taxpayer funding, sometimes many decades ago.She went further at the recent National Community Pharmacists Association (NCPA) meeting, where she expressed deep skepticism about PBMs:

There is nothing inevitable about the current structure of the market or the current business practices that occur and are permitted—these are all the result of policy and legal choices, that were made by public officials, and that can also be remade by public officials through the democratic process.”

“We’re kind of looking at middlemen across the board to try to understand, how could we be making sure that these markets are really serving people and not just the narrow self interests of gatekeepers?”In my April analysis of PBM market share, I quipped: “So, you should prepare to live with our current PBM market’s golden rule: Whoever has the gold gets to make the rules.”

Commissioner Khan clearly wants different rules.

No comments:

Post a Comment