Below, I violate Vegas code and tell you what happened there. I offer reflections on my keynote session with Scott Gottlieb, share my experiences during the featured session, and highlight three crucial specialty industry trends.

You’ll also find a link to my general session slides and some fun photos.

Enjoy!

WELCOME BACK, BLOGGER

Asembia’s Specialty Pharmacy Summit remains the most important forum for learning, networking, and conducting business throughout the entire specialty marketplace. The 2022 event, which had more than 6,000 registered attendees, was significantly enhanced by the Wynn’s awesome new conference facilities.

I offer a huge Drug Channels thank you to Larry and Robert Irene for sustaining and growing a valuable annual event that unites all aspects of the specialty industry in a neutral forum. Kudos to the indefatigable Chris Benz for pulling it all together once again.

Unfortunately, pandemic protocols forced Asembia to skip the traditional evening party. I look forward to Encore Beach Club shenanigans in 2023!

CHATTING WITH DR. GOTTLIEB

I had the privilege of participating in a wonderful conversation with Scott Gottlieb, M.D. As many of you know, he is a former FDA commissioner, sits on Pfizer’s board of directors, and is a thoughtful observer and expert voice on the U.S. healthcare system. (That’s why Gottlieb is one of only three people I follow on Twitter.) ICYMI, I reviewed his recent book here: Drug Channels Recommends: “Uncontrolled Spread” by Scott Gottlieb

Here’s a picture of us on stage. Click here for more photos from our session.

[Click to Enlarge]

We had a wide-ranging discussion about COVID-19, the public health infrastructure, biosimilars, rebates, and much more. I was especially intrigued by his insights about Aduhelm and the ensuing controversy over accelerated approval. He observed that the Centers for Medicare & Medicaid Services (CMS) has quietly created new policies that could have crucial implications for future specialty drug launches.

If you missed the session, I suggest Managed Healthcare Executive’s coverage of his commentary: Scott Gottlieb Covers the Bases: COVID-19, the CDC, Aduhelm, Biosimilars and Rebates.

THE UPDATE AND OUTLOOK

I also had the honor of presenting during the event’s general session: The Specialty Pharmacy Industry Update & Outlook. As in past years, I was joined by Doug Long from IQVIA.

You can download our full slide deck here: https://drugch.nl/asembia22.

I also made our slides available in real time at the conference via Twitter and LinkedIn.

If you were there on Tuesday morning, you heard us answer audience questions submitted by email during the session. And of course, we took a selfie from the stage—an Asembia tradition! (Bonus: You can see Paula, my wife and business partner, in the front row.)

[Click to Enlarge]

You can read about our session here:

- The Changing Dynamics of Specialty Pharmacy, CoverMyMeds

- Specialty Pharmacy Controls Limit Patient Access, Fein and Long Explain, Managed Healthcare Executive

ADAM’S TAKEAWAYS ON THE STATE OF SPECIALTY PHARMACY IN 2022

Here are three additional observations, based on my conversations at the summit:

1) Vertically aligned channels are trying to get organized—or beginning to deintegrate.

During my session, I reviewed the current vertical integration strategies of the large insurer/PBM/specialty pharmacy/provider companies and of hospital/specialty pharmacy/physician organizations. Many people told me privately about their own companies’ challenges when simultaneously being a supplier, partner, competitor, and/or customer of the mega channel players.

These vertically integrated companies touch many aspects of the channel and are searching aggressively for meaningful synergies. Consequently, manufacturers had to send large and diverse teams to Asembia. These included people from nearly all aspects of their commercial operations: market access, trade, medical affairs, patient services, pricing, contracting, and more.

However, some of the vertically integrated companies have started to unwind their vertical efforts. I noted the deintegration efforts of Centene, Prime Therapeutics, and Humana. (See page 9 of my slides.)

Looking ahead, I expect specialty pharmacies’ functions and profit models to be linked more closely to their parent organizations. This surely will be a hot topic at next year’s summit.

These vertically integrated companies touch many aspects of the channel and are searching aggressively for meaningful synergies. Consequently, manufacturers had to send large and diverse teams to Asembia. These included people from nearly all aspects of their commercial operations: market access, trade, medical affairs, patient services, pricing, contracting, and more.

However, some of the vertically integrated companies have started to unwind their vertical efforts. I noted the deintegration efforts of Centene, Prime Therapeutics, and Humana. (See page 9 of my slides.)

Looking ahead, I expect specialty pharmacies’ functions and profit models to be linked more closely to their parent organizations. This surely will be a hot topic at next year’s summit.

2) There are more specialty pharmacy buyers than sellers.

The shakeout and consolidation of smaller specialty pharmacies, combined with manufacturer and payer strategies, has concentrated dispensing in a handful of companies. See DCI’s Top 15 Specialty Pharmacies of 2021—And Three Factors That Will Reshape 2022.

Despite this reality, financial buyers prowled the summit, looking to buy a strong platform business. However, the larger independent specialty pharmacies are larger and generally well-capitalized, so prices will be steep.

On the final day of the conference, news broke of two notable transactions:

Despite this reality, financial buyers prowled the summit, looking to buy a strong platform business. However, the larger independent specialty pharmacies are larger and generally well-capitalized, so prices will be steep.

On the final day of the conference, news broke of two notable transactions:

- A group of private equity firms bought PANTHERx Rare from Centene, which had owned the business for less than 18 months.

3) Hospitals are resetting their specialty pharmacy strategies.

As I noted during my keynote, hospitals and health systems have emerged as the fastest-growing participants in the specialty pharmacy market. They accounted for nearly one out of five accredited specialty pharmacies. (See Exhibit 50 of our 2022 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers.)

Hospitals’ power is also growing as they acquire more physician practices and directly employ more physicians. They are becoming bolder about steering patients to in-house specialty pharmacies.

Hospital-owned pharmacies are able to generate significant profits by participating directly in the 340B Drug Pricing Program. In response to changes in manufacturers’ policies regarding external contract pharmacies, hospitals have accelerated their investments in in-house specialty pharmacy operations.

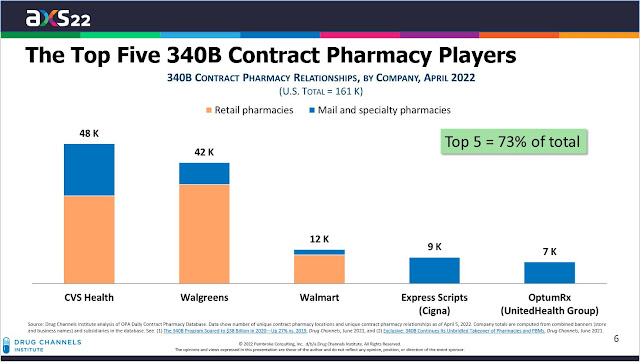

Ironically, the 340B kerfuffle is also encouraging hospitals to deepen their relationships with PBMs. When forced to choose a single contract pharmacy partner, hospitals and health systems have been gravitating to the large PBM-owned specialty pharmacies that have access to drugs in limited dispensing networks. As you can see in page 6 of my general session slides, PBMs now dominate the 340B contract pharmacy business.

THANK YOU, DEAR READERS!

Hospitals’ power is also growing as they acquire more physician practices and directly employ more physicians. They are becoming bolder about steering patients to in-house specialty pharmacies.

Hospital-owned pharmacies are able to generate significant profits by participating directly in the 340B Drug Pricing Program. In response to changes in manufacturers’ policies regarding external contract pharmacies, hospitals have accelerated their investments in in-house specialty pharmacy operations.

Ironically, the 340B kerfuffle is also encouraging hospitals to deepen their relationships with PBMs. When forced to choose a single contract pharmacy partner, hospitals and health systems have been gravitating to the large PBM-owned specialty pharmacies that have access to drugs in limited dispensing networks. As you can see in page 6 of my general session slides, PBMs now dominate the 340B contract pharmacy business.

[Click to Enlarge]

Thanks to the many Drug Channels readers who introduced themselves at the summit. I remain gratified by your compliments and words of encouragement.

Paula and I are glad that Drug Channels Institute remains useful and valuable to people throughout the industry. Below is a picture of us enjoying dinner at Mizumi.

[Click to Enlarge]

We’ll see you at #Asembia23!

No comments:

Post a Comment