Our analysis again reveals that despite what you may have heard, many independent pharmacies continue to hang on in a highly challenging retail environment. Prescription profits remained stable, while the average pharmacy owner’s salary jumped for the second year.

Read on for the financial details. The U.S. retail pharmacy industry faces many powerful headwinds. But there are some emerging positive trends, including DIR reform and profits from COVID-19 vaccinations. Expect independents to keep hanging in there.

MEET THE DATA

We again draw upon data from the National Community Pharmacists Association (NCPA) Digest, Sponsored by Cardinal Health. Click here to read the press release.

The digest presents selected 2020 financial and operating data submitted by pharmacy owners. These data have strengths and weaknesses. They do, however, provide the only publicly available, consistently published look at the financial position of independent pharmacies.

NCPA also collects more detailed financials, but it doesn’t share those data with external analysts. Since I don't have access to the complete financial report, some of the figures below are our estimates. However, for the first time, NCPA has graciously shared details on prescription profits. Based on these data, we have made slight restatements to the historical figures that were presented in previous articles.

PROFIT PRIMER

A pharmacy’s revenues come from prescription drugs, over-the-counter products, vitamins, cosmetics, groceries, and other merchandise. A typical independent pharmacy generates more than 90% of its revenues from prescriptions.

Here are some basic definitions to clarify the pharmacy profit story:

- Gross profit equals a pharmacy’s revenues minus the cost of products (net of discounts and returns) bought from a manufacturer or a wholesaler. Gross margin expresses gross profit as a percentage of revenues.

Gross profit measures the portion of revenues available for operating expenses and operating profit. Operating expenses include: (1) payroll expenses—the wages, taxes, and benefits paid to the pharmacy’s staff, including the business owners, and (2) general business expenses—everything else needed to run the pharmacy, such as rent, utilities, licenses fees, insurance, advertising, and other business costs.

- Operating income equals gross profits minus operating expenses. To be profitable, a drugstore’s gross profits must exceed its operating expenses. For example, a pharmacist-operated drugstore could report an apparent “net loss” if the pharmacy owner chose to pay himself or herself a larger salary instead of reporting a positive net profit.

- Owner's discretionary profit (ODP) equals the sum of the owner’s compensation and the pharmacy’s operating income. The NCPA digest formerly reported the ODP, but it has hidden the figure in recent years.

FAB FIVE

Here are five observations on the latest data:

1) Overall independent pharmacy profit margins remain stable.

In 2020, independent pharmacies' overall gross margin from prescription and non-prescription products was 21.9%. That’s comparable to the figures from the previous four years, which ranged from 21.8% to 22.0%.

This year’s findings differ slightly from U.S. government statistics, which show higher overall gross margins at chain and independent drugstores. For 2020, the drugstore industry’s overall average gross margin as reported by the U.S. Census Bureau was 24.4%. (source) The overall industry margin is higher than the independent pharmacy margin because non-prescription front-end products with higher-gross margins account for a greater share of sales at chain drugstores.

This year’s findings differ slightly from U.S. government statistics, which show higher overall gross margins at chain and independent drugstores. For 2020, the drugstore industry’s overall average gross margin as reported by the U.S. Census Bureau was 24.4%. (source) The overall industry margin is higher than the independent pharmacy margin because non-prescription front-end products with higher-gross margins account for a greater share of sales at chain drugstores.

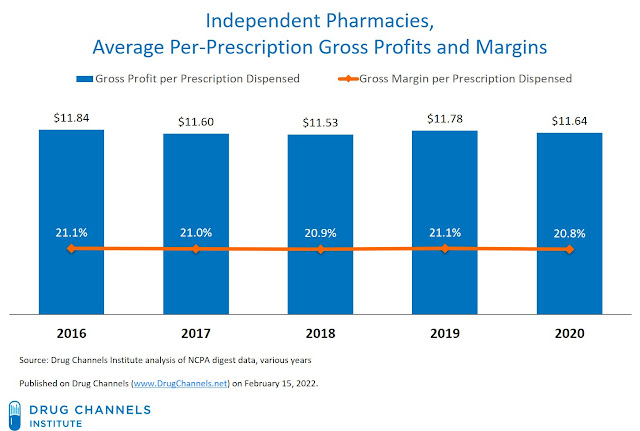

2) Independent pharmacies’ prescription profit margins are also stable.

For 2020, gross margins on prescription sales were 21.2%. As you can see in the chart below, prescription gross margins have been remarkably stable over the past five years.

[Click to Enlarge]

In 2020, the average per-prescription revenue in the NCPA sample was $55.96, roughly comparable to the $55.86 per prescription figure for 2019. For 2016 to 2020, gross profit per prescription has ranged from $11.50 to $12.00.

3) Independent pharmacies’ generic dispensing rates lagged those of the overall market.

The NCPA digest continues to record an odd discrepancy. For independent pharmacies, the generic dispensing rate (GDR)—the percentage of prescriptions dispensed with a generic drug instead of a branded drug—has lagged that of the overall market.

IQVIA data show that for 2020, the GDR for unbranded generics in the overall market was 88.5%. The NCPA Digest reports that the GDR for independent pharmacies was only 86% for 2020.

IQVIA data show that for 2020, the GDR for unbranded generics in the overall market was 88.5%. The NCPA Digest reports that the GDR for independent pharmacies was only 86% for 2020.

4) The average pharmacist who owned a single pharmacy earned about $158,000 in 2020.

We estimate that on a per-pharmacy basis, the owner’s discretionary profit (ODP) shrank from about $200K in 2015 to $129K in 2018. Since then, compensation has rebounded, to an estimated $141,000 in 2019 and $158,000 in 2020.

The increase came from better expense control, not higher prescription volume. For 2020, the average annual prescription volume per pharmacy in the NCPA sample was lower than the 2015 figure. However, total non-owner payroll expenses also dropped, which offset the lost gross profit from the lower prescription volume per pharmacy in the NCPA sample.

The salary gap between a pharmacy owner and an employed pharmacist has become smaller than it once was. However, this gap has expanded over the past few years. For 2020, the average gross base salary for a pharmacist at a retail, mail, long-term care, and specialty pharmacy was about $124,000. See Pharmacist Job Market in 2020: Hospital Employment Up, Retail Salaries Down.

In other words, owning a pharmacy, with all of its hassles and obligations, has again become more remunerative than being an employee.

The increase came from better expense control, not higher prescription volume. For 2020, the average annual prescription volume per pharmacy in the NCPA sample was lower than the 2015 figure. However, total non-owner payroll expenses also dropped, which offset the lost gross profit from the lower prescription volume per pharmacy in the NCPA sample.

The salary gap between a pharmacy owner and an employed pharmacist has become smaller than it once was. However, this gap has expanded over the past few years. For 2020, the average gross base salary for a pharmacist at a retail, mail, long-term care, and specialty pharmacy was about $124,000. See Pharmacist Job Market in 2020: Hospital Employment Up, Retail Salaries Down.

In other words, owning a pharmacy, with all of its hassles and obligations, has again become more remunerative than being an employee.

5) The NCPA now counts fewer independent pharmacies.

The NCPA has changed its methodology for counting the total number of independent community pharmacies.

For 2019, NCPA relied on “NCPA analysis of NCPDP data and NCPA research” to count 21,683 independent pharmacy locations.

But beginning with the 2021 edition, NCPA has switched to IQVIA’s data on U.S. retail pharmacy locations. For 2020, NCPA reports 19,397 independent pharmacy locations, which is more than one-third of all retail pharmacy locations.

There is still little evidence that independent pharmacies are vanishing. Independents have been losing overall market share, though total revenues for this dispensing format have been relatively stable. DCI’s analysis of IQVIA data show that the total number of independent pharmacy locations has held relatively stable over the past 20 years. Over the past five years, however, the number of independent pharmacies has trended downward—along with the total number of U.S. retail pharmacy locations. (See Section 2.3. of our pharmacy/PBM report.)

For 2019, NCPA relied on “NCPA analysis of NCPDP data and NCPA research” to count 21,683 independent pharmacy locations.

But beginning with the 2021 edition, NCPA has switched to IQVIA’s data on U.S. retail pharmacy locations. For 2020, NCPA reports 19,397 independent pharmacy locations, which is more than one-third of all retail pharmacy locations.

There is still little evidence that independent pharmacies are vanishing. Independents have been losing overall market share, though total revenues for this dispensing format have been relatively stable. DCI’s analysis of IQVIA data show that the total number of independent pharmacy locations has held relatively stable over the past 20 years. Over the past five years, however, the number of independent pharmacies has trended downward—along with the total number of U.S. retail pharmacy locations. (See Section 2.3. of our pharmacy/PBM report.)

NOT TOADALLY BAD

The challenging nature of retail pharmacy should not surprise readers of Drug Channels Institute’s annual economic reports.

Retail pharmacies are experiencing a period of intense competition that continues to pressure prescription profits. After years of stability, the number of U.S. pharmacy locations across all formats is trending downward. In CVS Pharmacy Downsizes: 10 Industry Trends Driving the Retail Shakeout, I outlined the many powerful headwinds facing retail pharmacy.

There are, however, some tailwinds benefiting pharmacies’ economics:

- COVID-19 vaccinations have generated significant—and well-earned—profits for retail pharmacies. About 41,000 retail pharmacy locations participate in the Federal Retail Pharmacy Program for COVID-19 Vaccination. It includes all major retail chains and many independent pharmacy networks. As of early February, pharmacies have administered about 227 million doses in the U.S. and accounted for more than 40% of all COVID-19 vaccines doses administered in 2021.

Pharmacies currently earn $40 per dose administered. Since a pharmacy incurs no cost of goods for a COVID-19 vaccine, the gross profits are equal to the administration fees. For example, a pharmacy earns a gross profit of $80 for administering a two-dose vaccine regimen. That’s why CVS Health’s retail pharmacy business earned more than $1.8 billion in operating profits from COVID-19 vaccines and tests in 2021.

- The Centers for Medicare & Medicaid Services (CMS) has proposed a new rule that would apply all pharmacy DIR price concessions to the negotiated price in Part D. The CMS rule would have multiple effects on Part D costs, including a small, positive impact on pharmacy economics. If the DIR were to be implemented as proposed, CMS estimates that pharmacies’ net Part D reimbursements will increase by only 0.1% to 0.2%.

Finally, a friendly reminder to my independent pharmacy readers: I'm not a magic wizard. I haven't caused these changes. I'm merely reporting on the facts and observing what's going on. Rather than getting hopping mad at me on Twitter, I suggest that you reflect on the business strategies that you will need to survive a highly challenging environment.

No comments:

Post a Comment