This week, I’m rerunning some popular posts while I prepare for today’s live video webinar: Discount Cards, Cost-Plus Pharmacies, and PBMs: Trends, Controversies, and Outlook.

This week, I’m rerunning some popular posts while I prepare for today’s live video webinar: Discount Cards, Cost-Plus Pharmacies, and PBMs: Trends, Controversies, and Outlook.Click here to see the original post and comments from January 2023.

For 2022, brand-name drugs’ net prices dropped for an unprecedented fifth consecutive year. What’s more, after adjusting for overall inflation, brand-name drug net prices plunged by almost 9%.

The factors behind declining drug prices will remain in the coming years—and become even stronger due to forthcoming changes in Medicare and Medicaid. Employers, health plans, and PBMs will determine whether patients will share in this ongoing deflation.

Read on for details and make up your own mind. And please pass the news along to the drug pricing flat earthers (#DPFE) who refuse to accept that brand-name drug prices are falling—or that prescription drug spending is a small and stable portion of overall U.S. healthcare expenditures.

Even a purple gorilla professor understands these facts.

DATA DISAMBIGUATION

To examine drug pricing, we again rely on data from SSR Health, an independent organization that collects and reports data on pharmaceutical prices. SSR Health is widely regarded as the leading provider of these data. In a testament to SSR Health’s influence, the Institute for Clinical and Economic Review (ICER) relies on these net price data in its cost-effectiveness evaluations. Click here to learn more about SSR Health and its US Brand Rx Net Pricing Tool.

SSR Health’s list and estimated net pricing figures are based on approximately 1,000 brand-name drugs with disclosed U.S. product-level sales from approximately 100 currently or previously publicly traded firms. The products and companies in the SSR Health numbers account for more than 90% of U.S. branded prescription net sales. SSR Health updates these figures quarterly, and its historical figures date from the first quarter of 2007.

Here’s DCI's quick refresher on drug pricing terminology:

- The manufacturer of a drug establishes the drug’s list (gross) price, called the Wholesale Acquisition Cost (WAC). A manufacturer’s gross revenues equal its revenues from sales at a drug’s WAC list price.

- A drug’s net price equals the actual revenues that a manufacturer earns from a drug after rebates, discounts, and other reductions. A drug’s net revenues equal its revenues from sales at the drug’s net price.

- Rebates to commercial payers, Medicare Part D plans, the Medicaid program, and other payers

- Discounts to healthcare providers under the 340B Drug Pricing Program

- Manufacturers’ payments to drug channel participants (admin fees to PBMs; fees and discounts to drug channel participants; and fees and discounts to pharmacies)

- Patient assistance and copayment support funds

DRUG PRICING REALITY CHECK

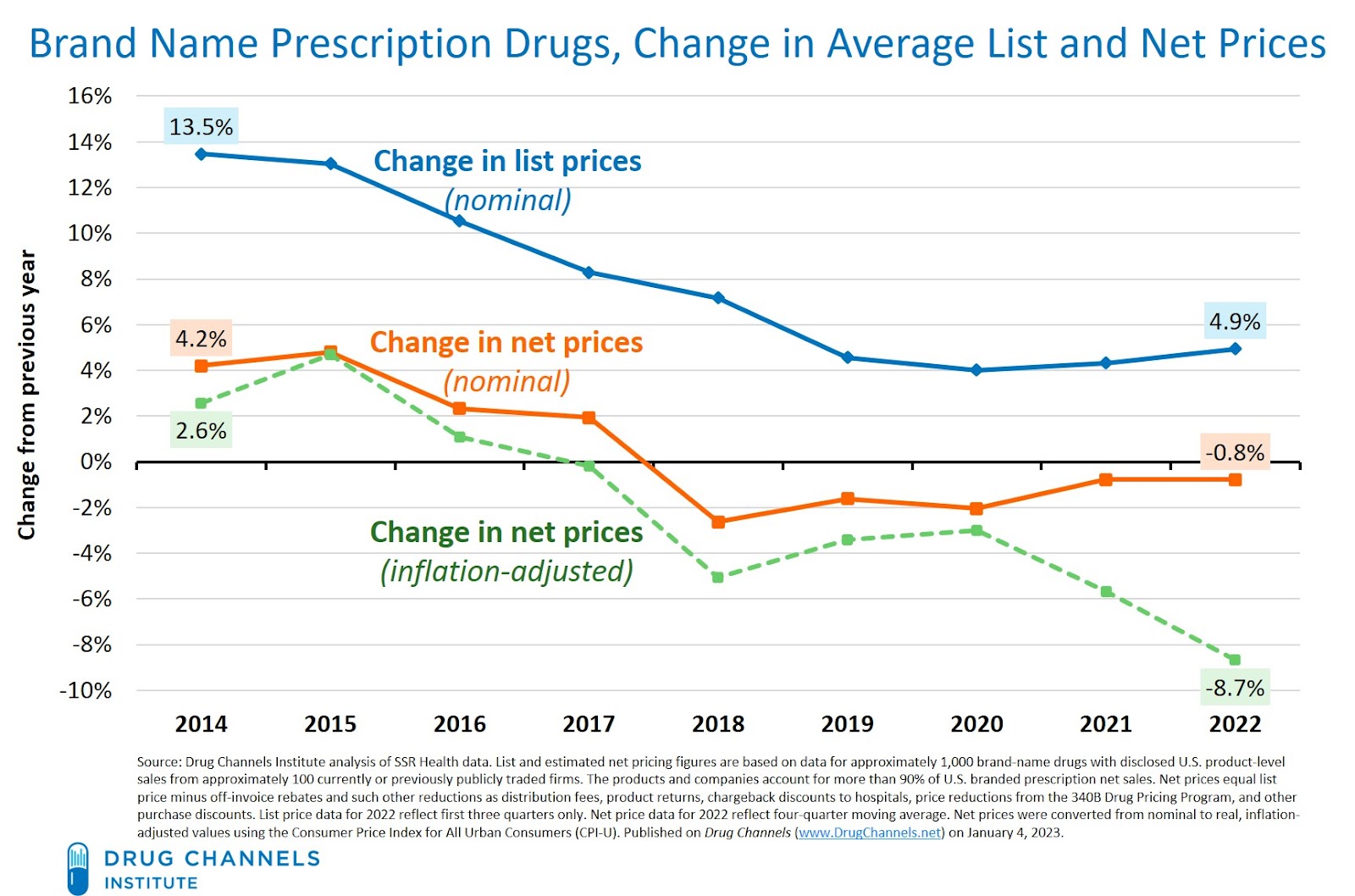

The chart below summarizes the list and net price changes for a broad set of brand-name drugs over the past nine years:

[Click to Enlarge]

Consistent with our previous analyses, these data show significant gaps between list and net price changes:

- List-price growth remains in the mid-single digits. From 2010 to 2015, growth in list prices was increasing by 10% to 15%. Growth has slowed sharply, from 13.5% in 2014 to 4.9% through the first three quarters of 2022. Average list price increases have been below 5% for the past four years.

According to early data compiled by 46Brooklyn, (unweighted) list price growth in 2023 remains at about 5%.

- Net prices for brand-name drug prices dropped for the fifth year. Through the first three quarters of 2022, net prices declined by -0.8%. The gross-to-net gap in prices was therefore -5.7% (= -0.8% minus 4.9%).

These industry data are consistent with the manufacturer-specific disclosures about changes in list and net drug prices that I discussed in Gross-to-Net Bubble Update: 2021 Pricing Realities at 10 Top Drugmakers. For 2021, list prices at 10 large manufacturers grew by 3.5%, while net prices declined by -1.0%. The unweighted average gross-to-net gap in prices was -4.5%. (Note that SSR’s figures are sales-weighted, while the manufacturer-specific figures reflect the unweighted average.)

- Net prices plummeted after adjusting for overall inflation. The consumer price index rose by more than 8% during the first three quarters of 2022—the time period shown in the chart above. (The inflation rate has since decreased slightly.) This means that real, inflation-adjusted list prices dropped by -3.4%, while real net prices fell by -8.7%.

- The gross-to-net bubble keeps inflating. Drug Channels Institute coined the term gross-to-net bubble to describe the dollar gap between gross sales at brand-name drug list prices and their sales at net prices after rebates and other reductions. We use “bubble” to characterize the speed and size of growth in the total dollar value of manufacturers’ gross-to-net reductions. (We have also anointed SpongeBob SquarePants as the honorary mascot of the bubble.)

Through the compounding effect of gross-to-net pricing differences, the total value of manufacturers’ off-invoice discounts, rebates, and other price concessions for patent-protected brand-name drugs continues to expand.

Consider a product launched in 2013 with a list price of $100 and no discounts or rebates. Its list and net prices would be equal, at $100. Using the average industry growth figures shown above, this product’s list price would have grown to $196 by 2022, while its net price would have been only $106. The difference of $90 (-46%) reflects the rebates and discounts that the manufacturer paid. These figures represent a lower bound, because newly launched brands always have some rebates and discounts.

That’s why for 2021, the total value of gross-to-net reductions for patent-protected brand-name drugs exceeded $200 billion. Unfortunately, the magnitude of the gross-to-net bubble reflects—and drives—both patients’ affordability problems, intermediaries' warped incentives, and politicians’ misunderstandings of U.S. drug prices.

As I discussed during the Drug Channels Outlook 2023 webinar, net price pressures will persist during 2023 and 2024. The factors behind ongoing gross-to-net differences include (but are not limited to):

- A highly concentrated PBM industry

- Aggregation of PBM rebate negotiations via group purchasing organizations

- The biosimilar boom (including the imminent launch of Humira biosimilars)

- Crowded, highly competitive therapeutic categories

- Payers’ widespread adoption of copay accumulator adjustment and copay maximizers

- Ever-expanding formulary exclusion lists (2023 update coming soon!)

- Skyrocketing growth in 340B Drug Pricing Program discounts

- Rebates and discounts to government payers

But wait, there’s more! In 2024, the Medicaid rebate cap will be removed, so products with years of list (not net) price increases will have rebates greater than 100%. Believe it or not, manufacturers will have to pay the government when their products are used by Medicaid patients. Crazy.

Despite what you may heard, net spending on pharmaceuticals accounts for about 15% of U.S. healthcare spending—yet somehow still absorbs 99% of the political heat and attention. Drugs’ share of U.S. health care spending is comparable to—or lower than—their share in other countries.

I recognize that relying on “facts” and “data” has become unfashionable. But here at Drug Channels, I remain guided by the late senator Daniel Patrick Moynihan's famous aphorism: "Everyone is entitled to his own opinion, but not his own facts."

No comments:

Post a Comment