Drug Channels delivers timely analysis and provocative opinions from Adam J. Fein, Ph.D., the country's foremost expert on pharmaceutical economics and the drug distribution system. Drug Channels reaches an engaged, loyal and growing audience of more than 100,000 subscribers and followers. Learn more...

Showing posts with label Mergers and Acquisitions. Show all posts

Showing posts with label Mergers and Acquisitions. Show all posts

Tuesday, August 19, 2025

Drug Channels News Roundup, August 2025: White Bagging Battles, Private Label Price Hypocrisy, 340B Patient Problems, and UnitedHealth Group’s Woes

Thursday, June 19, 2025

Mapping the Vertical Integration of Insurers, PBMs, Specialty Pharmacies, and Providers: DCI’s 2025 Update and Competitive Outlook (rerun)

This week, I’m rerunning some popular posts while I prepare for tomorrow's live video webinar: What’s Next for Retail Pharmacy: Data, Debate, and Disruption. I’ll be joined by special guest Antonio Ciaccia, CEO of 46brooklyn Research, and President of 3 Axis Advisors.

Click here to see the original post from April 2025.

It's time for Drug Channels’ annual update of vertical integration among insurers, PBMs, specialty pharmacies, and healthcare services within U.S. drug channels. As you can see below, we have revised, renovated, and refurbished our infamous illustration of the major vertical business relationships among the largest companies.

It's time for Drug Channels’ annual update of vertical integration among insurers, PBMs, specialty pharmacies, and healthcare services within U.S. drug channels. As you can see below, we have revised, renovated, and refurbished our infamous illustration of the major vertical business relationships among the largest companies.

Proponents of these vertical integration arrangements argue that they create opportunities to mine healthcare costs. However, these organizations remain highly controversial, due to the potential for anti-competitive behavior. We summarize some of the key issues below.

While some major companies have narrowed their focus or unwound previous integration efforts, ongoing consolidation and selective deconsolidation will continue to reshape the healthcare biome by trying to build something epic, block by block.

Click here to see the original post from April 2025.

Proponents of these vertical integration arrangements argue that they create opportunities to mine healthcare costs. However, these organizations remain highly controversial, due to the potential for anti-competitive behavior. We summarize some of the key issues below.

While some major companies have narrowed their focus or unwound previous integration efforts, ongoing consolidation and selective deconsolidation will continue to reshape the healthcare biome by trying to build something epic, block by block.

Wednesday, April 09, 2025

Mapping the Vertical Integration of Insurers, PBMs, Specialty Pharmacies, and Providers: DCI’s 2025 Update and Competitive Outlook

Proponents of these vertical integration arrangements argue that they create opportunities to mine healthcare costs. However, these organizations remain highly controversial, due to the potential for anti-competitive behavior. We summarize some of the key issues below.

While some major companies have narrowed their focus or unwound previous integration efforts, ongoing consolidation and selective deconsolidation will continue to reshape the healthcare biome by trying to build something epic, block by block.

What do you think? Click here to share your thoughts with the Drug Channels LinkedIn community.

Thursday, April 03, 2025

Vertical Integration Redux: How Pharmaceutical Wholesalers Are Transforming the Buy-and-Bill Market (rerun)

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar: PBM Industry Update: Trends, Challenges, and What’s Ahead.

This week, I’m rerunning some popular posts while I prepare for tomorrow’s live video webinar: PBM Industry Update: Trends, Challenges, and What’s Ahead.Click here to see the original post from February 2025.

In the video clip below, I review the vertical integration status of the largest three pharmaceutical wholesalers, illustrated in the chart below.

[Click to Enlarge]

I also:

- Explain how wholesalers have strengthened their position in buy-and-bill channels for provider-administered drugs through vertical integration with their downstream customers.

- Discuss how and why private equity roll-up activity has provided wholesalers with strategic opportunities to acquire ownership stakes in practice management companies.

- Outline the market access implications for provider-administered biosimilars in the buy-and-bill market.

For more on the forces of change affecting drug distribution and the buy-and-bill market, see Chapter 6 of DCI’s recent 2024-25 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors.

Monday, March 31, 2025

The Top Pharmacy Benefit Managers of 2024: Market Share and Key Industry Developments

For 2024, nearly 80% of all equivalent prescription claims were processed by three familiar companies: the CVS Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group. The names haven’t changed, but shifting relationships and contract shakeups have altered the plot, with Express Scripts stepping into a new lead role.

Below, we break down the latest market share data from Drug Channels Institute (DCI), explore the developments driving these changes, and examine what they signal for the future of the PBM landscape.

For a deeper dive into the state of the industry, join me this Friday, April 4, 2025, for our live video webinar: PBM Industry Update: Trends, Challenges, and What’s Ahead.

P.S. Special launch pricing on our new 2025 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers ends today (3/31/25)!

Tuesday, February 04, 2025

Vertical Integration Redux: How Pharmaceutical Wholesalers Are Transforming the Buy-and-Bill Market (Video)

In the video clip below, I review the vertical integration status of the largest three pharmaceutical wholesalers, illustrated in the chart below.

[Click to Enlarge]

I also:

- Explain how wholesalers have strengthened their position in buy-and-bill channels for provider-administered drugs through vertical integration with their downstream customers.

- Discuss how and why private equity roll-up activity has provided wholesalers with strategic opportunities to acquire ownership stakes in practice management companies.

- Outline the market access implications for provider-administered biosimilars in the buy-and-bill market.

For more on the forces of change affecting drug distribution and the buy-and-bill market, see Chapter 6 of DCI’s recent 2024-25 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors.

Wednesday, October 09, 2024

Five Crucial Trends Facing U.S. Drug Wholesalers in 2024 and Beyond

During this period of volatility, the core business model of the Big Three public pharmaceutical distribution companies—Cardinal Health, Cencora, and McKesson—remains intact. Put simply: Buy low, sell high, collect early, and pay late.

But as I explain below, wholesalers continue to position themselves as essential intermediaries by expanding their industry position and strengthening their economic fundamentals.

Read on for five key pricing, pharmacy, provider, and manufacturer trends that are driving the U.S. drug wholesaling industry.

For even more, check out DCI's new 2024-25 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors, the fifteenth edition of our deep dive into wholesale distribution channels.Click here to download a free report overview (including key industry trends, the table of contents, and a list of exhibits)

Monday, June 17, 2024

The Top Pharmacy Benefit Managers of 2023: Market Share and Trends for the Biggest Companies—And What’s Ahead (rerun)

This week, I’m rerunning some popular posts while I prepare for Friday’s live video webinar: The 340B Drug Pricing Program: Trends, Controversies, and Outlook.

Click here to see the original post from April 2024.

Three is still the magic number for pharmacy benefit managers (PBMs).

Three is still the magic number for pharmacy benefit managers (PBMs).

For 2023, nearly 80% of all equivalent prescription claims were processed by three companies: the Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group.

Read on for Drug Channels Institute’s (DCI’s) latest market share figures, along with a preview of the industry changes that will shift these shares over the next few years.

Click here to see the original post from April 2024.

For 2023, nearly 80% of all equivalent prescription claims were processed by three companies: the Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group.

Read on for Drug Channels Institute’s (DCI’s) latest market share figures, along with a preview of the industry changes that will shift these shares over the next few years.

Tuesday, May 07, 2024

Mapping the Vertical Integration of Insurers, PBMs, Specialty Pharmacies, and Providers: A May 2024 Update

Below you’ll find our latest illustration of the major vertical business relationships among the largest companies along with some of the notable activity since our previous update. These organizations continue to exert greater control over patient access, sites of care/dispensing, and pricing, although some have started to unwind their vertical efforts.

The companies face renewed scrutiny from the Federal Trade Commission, the Office of Inspector General, and members of Congress. But until anyone takes action, we will continue to live with the golden rule of the drug channel: Whoever has the gold gets to make the rules.

Tuesday, April 09, 2024

The Top Pharmacy Benefit Managers of 2023: Market Share and Trends for the Biggest Companies—And What’s Ahead

For 2023, nearly 80% of all equivalent prescription claims were processed by three companies: the Caremark business of CVS Health, the Express Scripts business of Cigna, and the Optum Rx business of UnitedHealth Group.

Read on for Drug Channels Institute’s (DCI’s) latest market share figures, along with a preview of the industry changes that will shift these shares over the next few years.

Tuesday, March 26, 2024

Drug Channels News Roundup, March 2024: My $0.02 of CarelonRx/Kroger & CVS, Provider-Owned Pharmacies, Shady AFPs, 340B Deception, and Lilly’s GLP-1 Ad

- What the CarelonRx/Kroger specialty pharmacy deal means for CVS Health

- Provider-owned specialty pharmacies expand in Medicare

- Payers are not keen on shady alternative funding programs (AFP)

- Hospitals’ association spreads 340B misinformation

P.S. Join my nearly 54,000 LinkedIn followers for daily links to neat stuff.

What’s ahead for the drug channel? Find out during Drug Channel Implications of the Inflation Reduction Act, a new live video webinar with Adam J. Fein, PhD. Click here to learn more and reserve your spot at our April 5 webinar.

Thursday, December 14, 2023

The Battle for Oncology Margin: How Private Equity Enables Vertical Integration by Pharmaceutical Wholesalers (rerun)

This week, I’m rerunning some popular posts while I prepare for tomorrow’s Drug Channels Outlook 2024 live video webinar. Click here to see the original post from October 2023.

In case you haven’t noticed, private equity firms have displaced hospitals and health systems as the major acquirers of community oncology practices. These financial firms have assembled significant oncology practice management companies that are primed for purchase by drug channel participants.

In case you haven’t noticed, private equity firms have displaced hospitals and health systems as the major acquirers of community oncology practices. These financial firms have assembled significant oncology practice management companies that are primed for purchase by drug channel participants.

Below, I review recent M&A trends and then examine the strategic objectives behind the acquisition of private-equity-backed OneOncology by AmerisourceBergen (Cencora) and another financial buyer. As I explain, AmerisourceBergen (Cencora) gains significant strategic advantage from this transaction, which echoes a historical McKesson deal.

The Federal Trade Commission’s (FTC) has a newfound interest in the roll-up transactions that are creating practice management companies. Nonetheless, I expect this consolidation activity to continue—enabling a new round of vertical integration in the drug channel.

FYI: Today’s article is adapted from Section 6.3. (Future Trends for Buy-and-Bill Channels) of our new our 2023-24 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors, now available to download at special launch pricing.

Below, I review recent M&A trends and then examine the strategic objectives behind the acquisition of private-equity-backed OneOncology by AmerisourceBergen (Cencora) and another financial buyer. As I explain, AmerisourceBergen (Cencora) gains significant strategic advantage from this transaction, which echoes a historical McKesson deal.

The Federal Trade Commission’s (FTC) has a newfound interest in the roll-up transactions that are creating practice management companies. Nonetheless, I expect this consolidation activity to continue—enabling a new round of vertical integration in the drug channel.

FYI: Today’s article is adapted from Section 6.3. (Future Trends for Buy-and-Bill Channels) of our new our 2023-24 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors, now available to download at special launch pricing.

Tuesday, October 17, 2023

The Battle for Oncology Margin: How Private Equity Enables Vertical Integration by Pharmaceutical Wholesalers

Below, I review recent M&A trends and then examine the strategic objectives behind the acquisition of private-equity-backed OneOncology by AmerisourceBergen (Cencora) and another financial buyer. As I explain, AmerisourceBergen (Cencora) gains significant strategic advantage from this transaction, which echoes a historical McKesson deal.

The Federal Trade Commission’s (FTC) has a newfound interest in the roll-up transactions that are creating practice management companies. Nonetheless, I expect this consolidation activity to continue—enabling a new round of vertical integration in the drug channel.

FYI: Today’s article is adapted from Section 6.3. (Future Trends for Buy-and-Bill Channels) of our new our 2023-24 Economic Report on Pharmaceutical Wholesalers and Specialty Distributors, now available to download at special launch pricing.

Wednesday, May 10, 2023

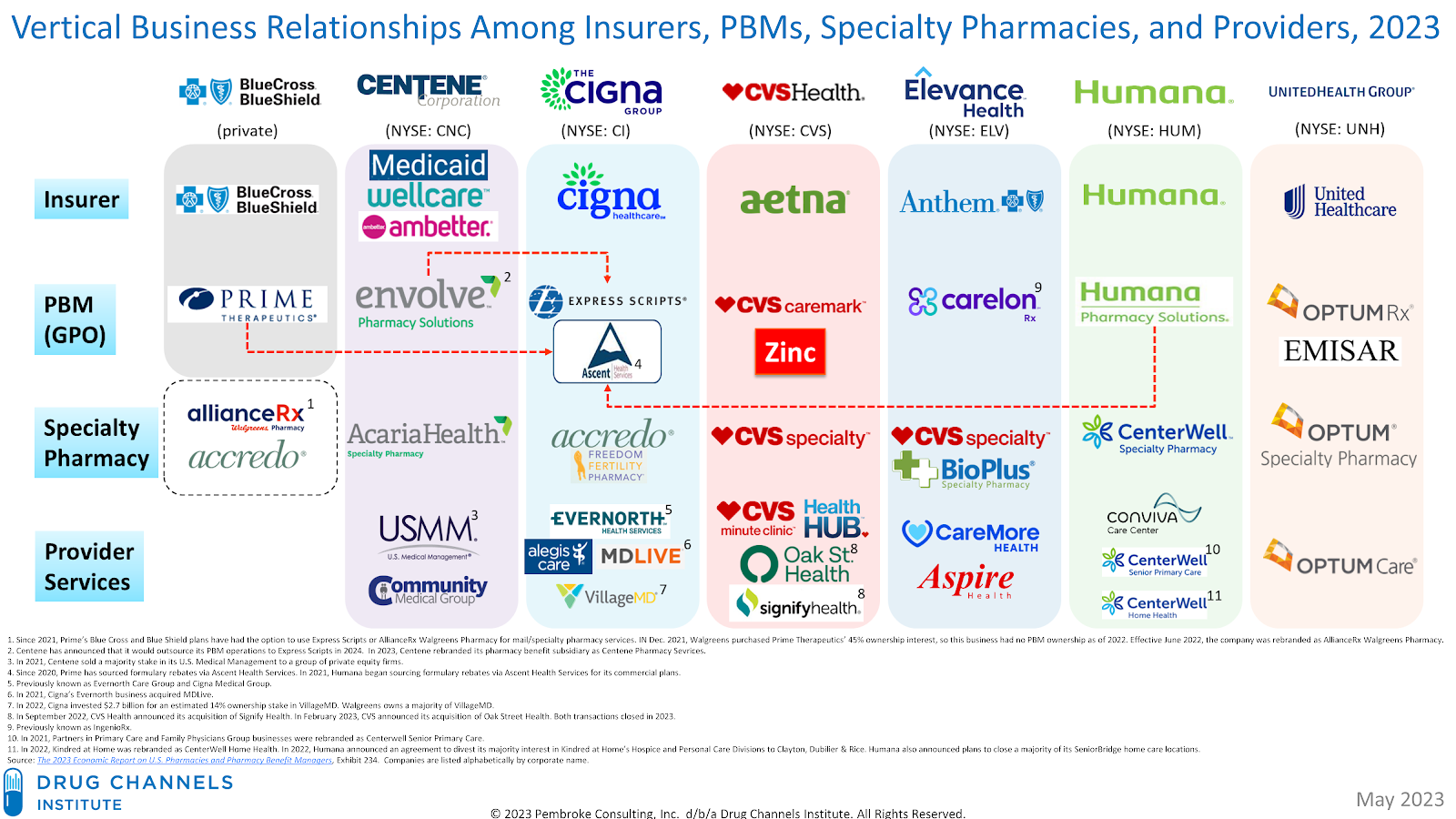

Mapping the Vertical Integration of Insurers, PBMs, Specialty Pharmacies, and Providers: A May 2023 Update

So, for your viewing and slide making pleasure, below you’ll find my latest illustration of the major vertical business relationships among the largest companies.

I estimate that at least half of all public and private U.S. healthcare spending flows through these seven familiar entities: Blue Cross Blue Shield, Centene, Cigna, CVS Health, Elevance Health, Humana, and United Health Group. Just like the heroes in Dawn of the Seven, they are here to serve and protect you.

Enjoy the artwork. In the meantime, I suspect that vertical integration may come up during today's Senate hearing on insulin.

Tuesday, January 17, 2023

Vertical Integration in Healthcare: 2023 Outlook for the Seven Major Players (Video)

In the brief video clip below, I review these businesses and offer some thoughts on their positioning for 2023. As you’ll see, the vertical strategy shakeout is underway.

If this clip whets your appetite for more, purchase a replay of the full 90 minute Drug Channels Outlook 2023 video webinar. Or register for my forthcoming 2023 video webinar series.

Tuesday, December 20, 2022

Drug Channels News Roundup, December 2022: Vertical Integration Updated, Walgreens vs. Pharmacy, Cash-Pay Rx, Curing 340B, and Deductible Season

Drug Channels also had a big 2022. We now have 35,000 LinkedIn followers, almost 25,000 email subscribers, and nearly 16,000 Twitter followers.

Thank you, dear readers, for welcoming me into your inboxes and browsers each week. I’ve had a blast writing Drug Channels and hope that you had fun reading it.

Wishing you and your family health and happiness,

Adam

Ring in 2023 with our final news roundup of the year:

- A vertical integration update

- Walgreens backs away from prescriptions

- Meet a cash-pay pharmacy that’s not owned by a billionaire

- Time to cure or kill 340B?

Thursday, October 13, 2022

Mapping the Vertical Integration of Insurers, PBMs, Specialty Pharmacies, and Providers: A 2022 Update

One is my chart showing the key channel flows within the entire U.S. pharmaceutical distribution, payment, and reimbursement system.

The other is my mapping of the insurer/PBM/specialty pharmacy/provider organizations that now dominate U.S. drug channels. Below, I provide an updated version of this second chart that reflects some recent transactions and name changes. About half of all U.S. healthcare spending flows through the seven companies shown below.

These organizations are poised to exert greater control over patient access, sites of care/dispensing, and pricing. But as I note below, Federal Trade Commission chair Lina M. Khan has other ideas about these companies.

Wednesday, July 27, 2022

DCI’s Top 15 Specialty Pharmacies of 2021—And Three Factors That Will Reshape 2022 (rerun)

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: Specialty Drugs Update: Trends, Controversies, and Outlook .

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: Specialty Drugs Update: Trends, Controversies, and Outlook .One update to the list below: CVS Health has quietly purchased AmerisourceBergen's US Bioservices specialty pharmacy.

Click here to see the original post from May 2022.

To complement that broader ranking, we present below our exclusive and updated list of the top 15 pharmacies based on specialty drug dispensing revenues in 2021. You will see that PBMs and insurers retained their dominance over specialty dispensing.

But as I explain below, 2022 will be a year of transition. Significant volume will shift to the larger players, as Centene plots its exit, Walgreens’ specialty pharmacy business collapses, and manufacturers’ 340B contract pharmacy restrictions continue.

This week, I’m attending Asembia’s Specialty Pharmacy Summit. In a future article, I’ll violate Vegas code and tell you what happened.

Monday, July 25, 2022

The Top Pharmacy Benefit Managers of 2021: The Big Get Even Bigger (rerun)

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: Specialty Drugs Update: Trends, Controversies, and Outlook.

This week, I’m rerunning some popular posts while I prepare for this Friday’s live video webinar: Specialty Drugs Update: Trends, Controversies, and Outlook.Click here to see the original post from April 2022.

Consider Drug Channels Institute's latest estimates of pharmacy benefit manager (PBM) market share, shown in the chart below. For 2021, we estimate that the three biggest PBMs accounted for 80% of total equivalent prescription claims. Significant business relationships among the largest companies continue to shift market share.

As I explain below, the prospects for market disruption remain low, so the controversial warped incentives of the rebate system will continue to distort the drug channel.

Tuesday, May 31, 2022

Drug Channels News Roundup, May 2022: SaveonSP Sued, RIP Medicaid Accumulator Rule, CVS/ABC Deal, Buy-and-Bill Profits, and Aetna’s Prior Authorizations

- SaveonSP gets sued

- Thoughts on the Medicaid accumulator rule opinion

- CVS buys AmerisourceBergen’s specialty pharmacy

- Fresh data on hospitals’ cancer drug profiteering

P.S. Join my more than 27,000 LinkedIn followers for daily links to neat stuff. You can also find my daily posts at @DrugChannels on Twitter, where I have more than 14,000 followers.