Below, we rely on a unique database to provide you with some never-before-published benchmarking data on manufacturer-defined networks for 290 specialty drugs.

As you’ll see, a typical network contains only five specialty pharmacies. However, this average disguises substantial variability in network size. More than one in four specialty products have an exclusive network, while some have as many as 25 participants.

Manufacturers almost always say “be mine” to pharmacy benefit manager (PBM) affiliated partners, but they also swipe right with unaffiliated specialty pharmacies. Alas, PBM and plan strategies can still make smaller pharmacies feel lonesome.

PICK ME

Manufacturers often limit and manage the specialty pharmacies eligible to dispense expensive specialty medications. A manufacturer can adopt one of two basic pharmacy channel strategies for its patient-administered specialty drugs:

- Open distribution. This channel strategy does not explicitly distinguish between specialty and traditional drugs. All pharmacies have access to open distribution products because they can be purchased from a wholesaler. Therefore, wholesalers can inventory, sell, and distribute these specialty products as they would traditional, nonspecialty drugs. Through open distribution, the manufacturer does not limit the number of pharmacies that can dispense its product.

Retail and other pharmacies have the greatest access to such open distribution specialty products because they can be purchased from a full-line wholesaler. Health plans and PBMs, however, typically limit pharmacies’ ability to dispense these open distribution products.

- Limited/exclusive dispensing network. In this approach, pharmaceutical manufacturers limit the number of specialty pharmacies authorized to dispense their specialty products. Manufacturers select pharmacies with the distinctive capabilities required to serve patients, providers, and payers efficiently and effectively. The manufacturer specifies the pharmacy locations that are eligible to dispense its product. Pharmacies that are excluded from a manufacturer’s network are unable to purchase and dispense a particular specialty product.

In some cases, the manufacturer may designate only one pharmacy to dispense to the entire patient population. An exclusive network is typically used when the patient population is small or whenever the product has significant safety issues.

I ♥ YOU, DATA

To characterize manufacturers’ specialty pharmacy networks, we relied on IPD Analytics’ Access Hub platform, which includes Limited Distribution Drug Network Tracking. This unique database tracks a broad universe of specialty drugs and their pharmacy networks. As far as I know, there is no comparable resource available for analyzing specialty pharmacy networks. To learn about this database and how you can get access, please contact Tim Powers (tpowers@ipdanalytics.com).

As of late December 2022, we found that IPD Analytics tracked 290 specialty drugs with a manufacturer-defined limited or exclusive specialty pharmacy network. We analyzed these data to identify the number and identity of specialty pharmacies in each product’s network. Products with multiple routes of administration or formulation, e.g., capsule vs. tablet, were treated a s single product. In all cases, the specialty pharmacy networks were identical regardless of drug formulation.

YOU + ME

The chart below summarizes the specialty pharmacy network size for 290 specialty drugs.

[Click to Enlarge]

The average network had five specialty pharmacies. However, this average disguised substantial variability in network size:

- More than one in four specialty drugs (28%) had exclusive dispensing networks, with only a single specialty pharmacy.

- A further 31% of networks had small, but nonexclusive, networks with two to four pharmacies.

- About one in four specialty drugs (24%) had networks with 5 to 10 specialty pharmacies. The average network size for these products was 7 pharmacies.

- About one in six products (16%) had a relatively larger network of 10 to 25 specialty pharmacies. The average network size for these products was 14 pharmacies.

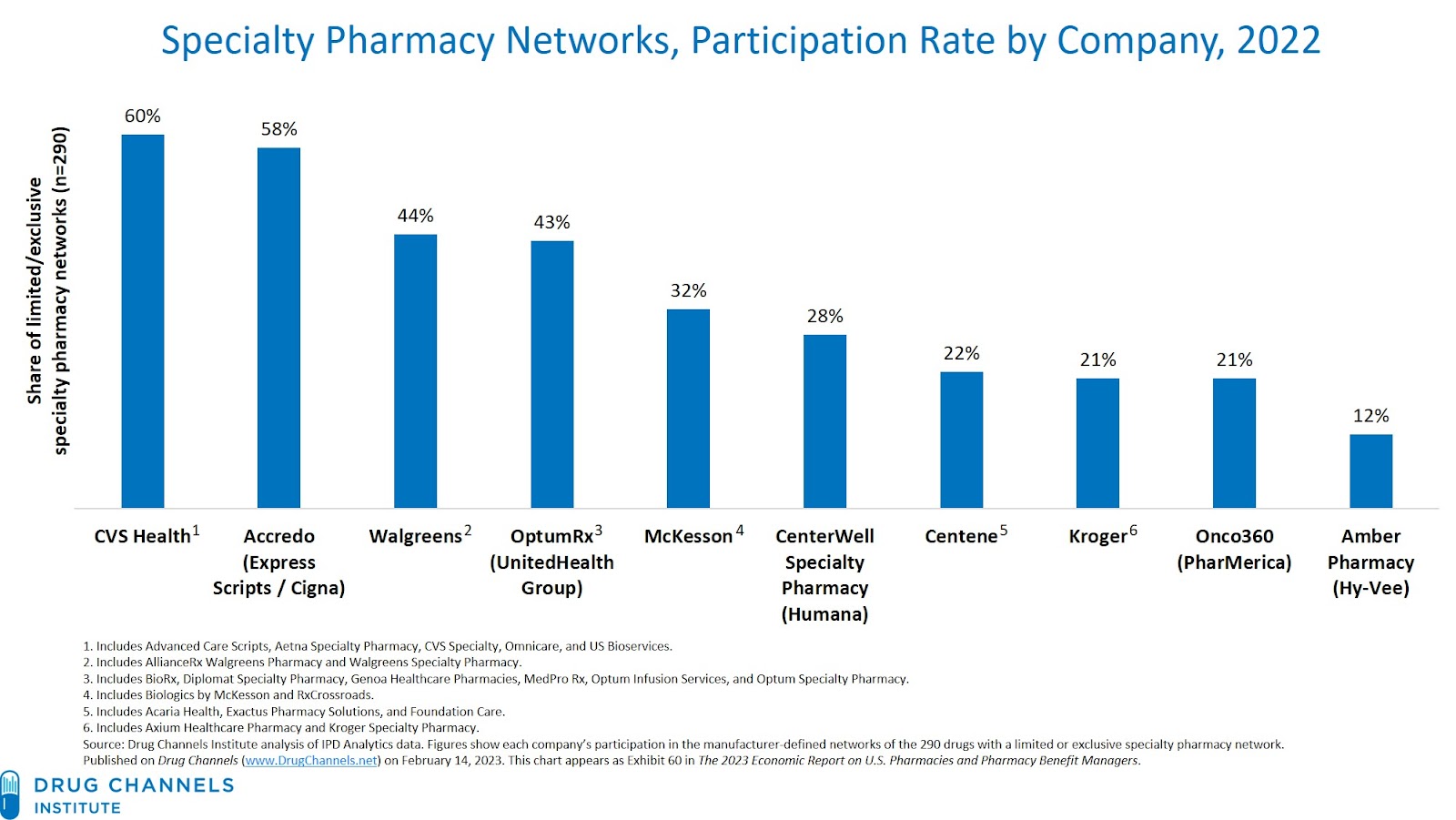

The chart below shows the 10 specialty pharmacies with the greatest access to the 290 specialty drugs that had a manufacturer-defined limited or exclusive specialty pharmacy network. The specialty pharmacies owned by the two largest PBMs—CVS Health and Express Scripts—had access to more than half of the specialty drugs in limited networks. Many of the country’s largest specialty pharmacies were only included in a minority of these products’ networks.

[Click to Enlarge]

We also examined the companies designated as the sole specialty pharmacy network participant for the 28% of products with exclusive networks. The pharmacies owned by the two largest PBMs accounted for 30% of all products with exclusive networks. However, smaller and independent specialty pharmacies were well-represented in exclusive networks. For example, McKesson’s Biologics and RxCrossroads pharmacies accounted for 22% of the exclusive-network drugs, while PANTHERx Rare Pharmacy accounted for a further 9% of these products.

BEAR HUG

Regardless of a manufacturer’s network, PBMs and their plan sponsors usually require patients to use the specialty pharmacy that the plan or PBM owns and operates. This has further shifted dispensing to the largest specialty pharmacies owned by vertically integrated organizations.

The concentration of specialty dispensing revenues that we have documented results from the dual strategies that plan sponsors and manufacturers use to narrow specialty drug channels. For smaller pharmacies, this combination is worse than getting an empty box of chocolates for Valentine's Day.

We’ll have additional romantic specialty market data in our forthcoming 2023 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers. Details next week!

No comments:

Post a Comment